Update: Brookfield investor day summaries

Transcript summaries of the Brookfield universe investor days

With my larger holdings, I manually summarise the transcripts from earnings calls and investor days. Obviously it would be quicker to get AI to do it, but I just don’t think you get the nuance that way, or the same clarity on what is changing over time and what isn’t.

Here are my summaries of the last Brookfield investor day transcripts. I hope they’re useful.

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

BN - real estate and Wealth Management are huge opportunities

19% CAGR over 30 years, or 27x.

Plan value today is $180bn or $68 per share. This is 16x average annual earnings over the next 5y and 10x average annual DE.

“I’m quite confident we can sell all the businesses for probably premiums to those numbers.”

$82bn is public holdings.

$12bn is funds managed by BAM, compounding at 15%. Will realise net $5bn over 5 years.

$34bn is PV of carry, valued as net unrealised carry + annual targeted carry x10. (They also do a DCF which produces the same result at an 8.5% discount rate.) They’ll convert $6bn to cash over the next 3 years and $25bn over the next 10, net.

$26bn is real estate.

$26bn is BWS at 15x annualised DE.

Expect 25% DE and 16% plan value CAGR for next 5 years.

5y DEPS target $6.95.

Will generate $53bn of cash flow over the next 5 years, I think including asset sales. $28bn will go to dividends and to grow BWS, $25bn is free to be reinvested.

Generating 15% returns is easier than it was due to scale and capabilities.

Nimble within two guiderails: value investing, and driving returns through operating capabilities.

“Once we understand an industry, we move fast and we deploy at scale. We’re not early, but once we understand it, we move fast and we deploy at scale.”

Real estate

Sold $5bn of balance sheet assets over the last year and refinanced $16bn.

Plan value $26bn and DE $730bn. Will sell $24bn over the next 5 years, reinvest $10bn, and generate $3bn in annual dividends, leaving 2030 plan value $15bn and DE $640m.

In the last year, balance sheet investments have signed 15msf of leases at 11% rental spreads. This will drive NOI over the next 2 years as leases roll. 5y NOI LFL CAGR should be 4%.

Now splitting assets into 3:

Super-core is 60% of invested equity. 34 irreplaceable and complex assets that they can keep reinvesting in and will own forever (but may sell stakes). 90% of this is office and retail with 95% occupancy and 47% LTV. 10% is resi and mixed use.

Core-plus is 25% of invested equity. 57 assets of equal quality to supercore, but with business plans that are complete or being completed and which will be sold. The performance metrics are almost identical to supercore: 27 office assets have 44% LTV and 94% occupancy.

Value add is 15% of invested equity. 95 assets generally in secondary markets where the plan is to reposition and sell.

Office: 2 years ago only 5% of companies required employees to be in the office all the time. Now it’s over 50%. 2 years ago the average work requirement was 2.5 days per week. Now it is almost 4 days. But nothing has been built for years, and existing supply is being converted to other uses. Very little space is available for new leases, so the premium for new office space averages 60% globally. In NYC it is over 100%.

Retail is driven by consumer spending. US retail spending is 140% of 2019 levels but there is virtually no retail construction - since 2015, US retail construction has focused on convenience and not shopping destinations. “This directly impacts retailers who are starved for more space.”

Alderwood Mall in Washington is 99% occupied with NOI up 50% since 2021. They’ve just refinanced at 5.9%, having recently redeveloped an old Sears box into 76ksf of retail space plus 328 apartments. The new retail space is 100% leased and generates $4m of NOI, while the apartments are 96% leased and have just been sold at a 4.7% cap rate.

Fashion Place in Salt Lake City is 100% leased and generates $1000psf in sales. Replacing underperforming brands has driven sales up 20% since 2021 and they have just refinanced at 5.4%.

Flatt: “I’ve seen [this cycle] 5 times before. The psyche got hurt more this time, but the fundamentals are actually way, way better as we come out of the bottom of the market”.

Brookfield Wealth Solutions

$135bn of assets, $14bn of equity, $1.7bn of DE ($2.1bn next year).

3 big recent transactions have been at an average of 1.8x book, which implies $26bn of value or $20 per share of BN.

Also generates $300m of fees to BAM on $30bn of assets invested in funds.

Including the UK acquisition they will have $180bn of assets, $30-35bn of inflows, $10bn of outflows, and $20-25bn of net inflows. Add some M&A and they can reach $350bn of assets and $5.5bn of DE in 5 years, reaching a 17% ROE and valued at 12-15x.

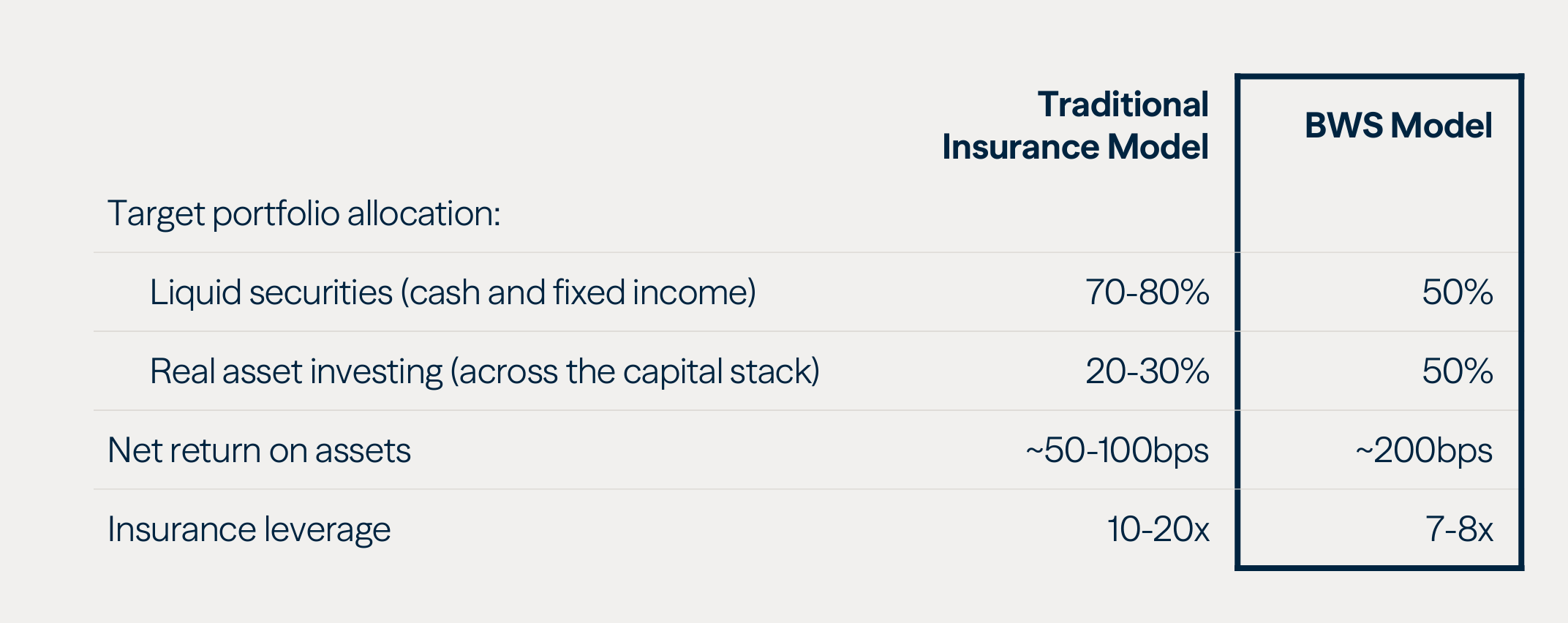

“Investment-led insurance” - by investing in high-yielding private assets, you can have low leverage and lots of cash. This combination is great for risk, returns, and regulators. Most insurers operate at 10-20x leverage. Brookfield operate at 7-8x and they have $50bn of assets in cash or cash equivalents. All their businesses have A ratings and 2 have had upgrades under Brookfield ownership due to retained capital.

“We think we can build a business that can compound capital for many decades to come” driven by aging and Brookfield’s ability to invest at scale.

Today 1 in 6 Americans are over 65. By 2050, it’s 1 in 4. Same all over the developed world. This plus the lack of DB pensions drives a $7tn retirement deficit.

Aging drives demand for wealth products.

Pensions and Sovereigns is a $22tn market.

Today US retirement accounts have $40tn (401ks, IRAs, and employer DC accounts). By 2040 this will be $100tn.

20 years ago 7% was in annuities; now 10%, and likely going to 15%.

Trump’s recent Executive Order opens retirement accounts to private assets.

Brookfield can offer high return private investments in the accumulation phase, and then competitive annuities for the decumulation phase.

Initially thought they would do this as a reinsurer and then realised the value of distribution. American National and American Equity previously did $5bn of annual annuity origination combined. Now they do $25bn with more to come - but they scale back when rates aren’t right.

Regulation is “an incredible moat”. They work hard with regulators “to make sure our disclosure is at the top end of their expectations and to default to overcommunication…the more we work with regulators, the more that moat widens and gives us protection and creates scarcity value”.

Massive value created by buying insurers at or below book, selling noncore lines for 1.6x, and then selling all their long dated bonds just before inflation took off.

BAM

FRE: $2.7bn today → 17% CAGR to $3.59/share by 2030.

DE: 18% CAGR. Base case 2x in 5 on $1.2tn FRE-bearing capital, “inherent operating leverage”, rapidly scaling complementary products.

Additional levers get to >20% DE growth.

Exceeded last 5-year plan: FRE-bearing capital $563bn vs $510bn target; FRE $2.7bn vs $2.6bn.

Carry drives growth after 2030.

87% of fee-bearing capital is long-term or permanent in nature, growing to 92% by 2030 — structural earnings visibility most peers can’t match.

Past 12 months: raised $97bn, deployed $135bn, monetised $75bn, returned $50bn - record monetisations despite low M&A volumes.

Competitive position.

Owner-operator model, co-investment alignment, and boots-on-ground operational expertise are the core differentiators.

Scale creates a self-reinforcing loop — platform attracts capital, capital enables better deals, deals build the track record.

Brookfield capital goes in first, clients come alongside.

Cross-platform information advantage: Westinghouse underwritten because of renewables expertise; Canadian housing underwritten because of real estate presence; Chemelex surfaced because of infrastructure knowledge.

Compounding expertise from repetition - hundreds of renewables deals, deep infra experience.

Growth levers

Products: >70% of fee revenue from strategies launched in the last decade. Lots more to come following the pattern flagship → complementary → retail.

Institutional share of wallet; although BAM is in 39 of the world’s top 50 investors, they only have 2% of their alts portfolio.

Partnerships: $40bn of go-forward deployment from bilateral partnerships announced in 2025 alone. Barclays partnership seeding financial infrastructure fund; sovereign AI partnerships seeding AI infrastructure fund. Partnerships are multi-dimensional — tenants, offtakers, pension managers, co-investors.

Individuals: private wealth raising $10bn this year, up 50% y/y. 60,000 private wealth clients vs zero 5 years ago. 401(k)/retirement markets are “early, early, early innings” this opening is not in their base case.

Europe institutional: expect to raise 3x 2024 levels in 2025 — “infancy.”

Family capital also barely started.

Outlook by business segment

Infrastructure: massive multi-year investment need. Spinning out dedicated AI infrastructure fund, which is differentiated because half is yielding, not greenfield, with sovereign and hyperscaler counterparties on 20yr+ contracts. US data centre vacancy <2.5%; 10GW of lease capacity added in US this year alone.

Renewables & Transition franchise now generates >$400m annual revenue, built in <5 years from zero. Largest transition strategy globally.

Real Estate: — fundamentals strong, supply near-zero, capital structures normalising, transaction activity recovering and rate cuts will accelerate this. Sold $3.7bn, deployed $6bn in last 12 months. “Rents going through the roof” in next 5 years. Buying multifamily at 5.7% caps (vs historically selling at 3.7%), with pathway to >7%. 20‑yr opportunistic track record: 21% gross / 17% net on $44bn equity.

Private Equity: 26% average gross IRR over 25 years across 6 vintages — “best performing PE track record in the market.” Wealth, structured equity, and financial infrastructure products on the way.

Credit & Castlelake: $250bn FBC today vs $100bn 5 years ago. Private credit is still very early and asset-backed finance is “taking off.” Capital markets business growing — 2-3 years to materiality but credit growth could accelerate that significantly.

AI and productivity

“Robotics and AI can soon change a lot of processes… margins will expand dramatically over time.”

“We are possibly in one of the greatest investment booms in history… leading to some of the greatest productivity advances we will ever see.”

M&A: 7 meaningful additions in 5 years (Oaktree, LCM, 17Capital, Primary Wave, Pinegrove, Castlelake, Angel Oak). Options allow buying ~$250m of incremental FRE over time.

BIP

L5y FFO/unit CAGR 10%

L5y understated true performance: FX headwind cost ~2% annually; rate headwind cost 2-3%. Adjusted for both, underlying growth was ~14%.

Targeting return to 14%+ long-term rate over next 5 years.

Distributions: target higher end of 5-9% target range, without increasing payout ratio (currently 67%, down from 78%).

2025 to date: deployed $2.1bn ($700m organic, $1.4bn new investments); recycled $2.8bn at 20% IRR / 4x MOIC - annual record and “exceptional” given these were regulated/contracted assets. Already at $3bn recycling target. Private market transactions achieved 15x EV/EBITDA — 3-4 turns above where BIP trades publicly.

Competitive position

Full-cycle strategy: deploy at 12-15% hurdle, crystallise value through recycling, maintain liquidity to go on offence in dislocations. COVID, rate shock, and the trade war produced some of BIP’s best acquisitions.

Cross-sector learning:

Intel semiconductor deal assembled from data centre contracting + LNG project finance + corporate partnership governance knowhow.

Hotwire identified as two businesses (development platform + stabilised portfolio) at signing - value not recognised by sellers.

100% of new investments funded internally over last 3-4 years - recycling makes BIP self-funding.

Private market buyers paying 10-11% cost of equity for BIP’s mature assets; BIP redeploying into 15-17% returning opportunities - spread is core compounding engine.

Growth levers

Organic backlog 4x larger than 5 years ago - highest-returning capital deployment.

Recycling program 5x larger, now $2-3bn annual run rate going forward.

AI infrastructure: $500m annual BIP deployment targeted.

Macro turning: rates stable/falling and USD softening for first time in years.

AI buildout

1-2% of US GDP, larger than the fiber build-out, approaching railroad-era scale, analogous to electric grid build-out in duration and necessity.

Power density per rack is 10x non-AI and forecast to rise 5-10x within 10y.

Data centre inventory sold out.

AI factories are DCs plus $30m/MW of chips - 4x the capital intensity of standard cloud.

Recent acquisitions

Colonial Pipeline: largest US refined products system, 50% of East Coast demand, 5,500 miles Houston-NY, 9x EBITDA with FERC-regulated inflation-linked tariffs and 90%+ utilisation. Bought during trade war noise with limited competition. Upside from operational improvement.

Hotwire: bulk fibre to HOAs, immediately recycled stabilised assets to lower-cost capital. Growth via homebuilder partnerships and Brookfield ecosystem.

BBU

Adjusted EBITDA $2.7bn, 5y CAGR 16%.

EBITDA margins doubled from 12% to 24%.

Adjusted EFO/unit: $3.65 → $6.90.

NAV: $28 in 2020 → $54 today.

Capital recycling: $2bn target for 24 months achieved in 12; confident of another $2bn over next 24. The sale of 3 partial interests at an 8.6% discount to Brookfield’s evergreen fund, if reinvested in buybacks at market prices, adds $2.50 in NAV/unit.

Long term record

26% gross / 20% net IRR over 25 years, driven by margin expansion, not multiple expansion or financial engineering.

Since IPO: 25 investments monetised, $8bn of proceeds at BBU share, in line with carrying NAV and above target returns.

Brookfield ecosystem ($1.1tn AUM, 400 companies, 30 countries) is the information advantage

Cross-portfolio best practices identified and deployed at scale.

AI use cases now live across 200+ applications; best practice in one company rolled to all 400.

AI value creation office: 30 dedicated people sharing lessons.

Buying industrial companies that benefit from AI as a productivity tool.

Clarios: custom ML algorithm on 30yr-old facility saved 60% more than expected, now rolling across all Clarios plants and comparable BBU businesses.

Sagen: ML models on 25 years of proprietary data — mortgage underwriting automation up 1.5x, better house price prediction, improved fraud detection.

Financial infrastructure is a new priority vertical.

$4tn market opportunity.

Strategy: buy asset-light software and services businesses (not banks), unshackle them from conglomerate parent constraints, digitise/automate, and deploy operational expertise.

Target characteristics: scale, distribution, technology-enabled, regulatory moat.

Network + Magnati combined into #1 payments provider in Middle East/Africa, processing >60% of regional payments.

Barclays payments carve-out: building “the largest startup you can imagine” — 3,000 people, every process being rebuilt from scratch. Target: $200m EBITDA uplift.

Now have leading payment infrastructure in 60+ countries.

Ranjan: “we can quadruple the EBITDA of these businesses soon after buying them.”

BEP

FFO/unit: 10% organic annual growth. Building blocks:

inflation escalation (~2%, $150m incremental FFO over 5 years)

re-contracting at higher prices ($100m)

asset optimisation (1-2%)

development pipeline execution ($385m, ~5%).

Competitive position

Only platform combining large-scale low-cost wind/solar with irreplaceable baseload — hydro, nuclear (Westinghouse), and now batteries (Neoen).

Hyperscalers need 99.999% availability; BEP can deliver both cheapest power and reliability, most peers can only do one.

Hydro: largest private portfolio globally. More strategic than ever - dispatchable, 24/7, scarce. Selectively recycling non-core assets (First Hydro UK, Maine portfolio) while reinvesting in core (increased Isagen stake). Google framework locks in long term contracted cash flows and enables up-financing; it is also is a “hunting licence” for US hydro M&A.

Nuclear: Westinghouse serves ~2/3 of world’s nuclear fleet, supplies ~half of all reactors globally = global scale + deep US expertise = ideal positioning for new builds, life extensions, and accelerating global investment. Still “very early stages of a long sustained investment cycle.”

Discipline as an edge: deliberately avoided offshore wind (subsidy-dependent, construction risk), residential solar (unproven economics), and highly leveraged structures.

“Clean portfolio, track record and balance sheet” entering the upswing. Highest credit rating in sector and financing terms improving - 10-year notes in March at lowest coupon in 5y, tightest spread in 20y.

Growth drivers

Data centres alone drive 8-10% annual US power demand growth through 2050.

Deployment: $9-10bn over next 5 years across development and M&A - step up from prior targets.

Half is now proprietary organic development.

Target adding 10GW annually by 2027, sustained from there.

Capital recycling now a core, recurring part of the model. Each portfolio company now recycles assets as they mature. Target >$2bn of asset sales annually.

M&A: pipeline >$100bn enterprise value. BEP wins on certainty of capital and execution speed, not price. Renewables regulatory uncertainty in US market is creating attractive entry points. $25bn of partner capital available alongside BEP’s own $4.7bn - total equity firepower ~$30bn.

Batteries: costs down 90% since 2010, further declines expected. Neoen acquisition makes BEP global leader - 1.5GW operating, ~50GW development pipeline. Fastest-growing segment within BEP. Firms up intermittent renewables to meet reliability demands, particularly for datacenters.

Wind and solar development are nearly the entire pipeline in key data centre markets. Contracting activity with hyperscalers up ~100% in last 2 years. Microsoft and Google partnerships - only two such framework agreements in the industry.

Opportunity to consolidate distributed generation: smaller renewable assets, typically solar, sited close to or at a commercial or industrial customer’s premises, with the power contracted directly to that offtaker. These ease grid constraints and deliver cheap power.

Capital recycling

Platforms: Saeta Yield, India platform, Luminace majority - 26% IRR, 2.6x MOIC.

Individual assets: First Hydro, Shepherd’s Flat, Maine hydros - 18% IRR, 3x MOIC.

Links to previous work

Thanks for reading - if you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete

Thank you! Really nice. Any commentary on the private credit narrative with respect to non accruals and software valuations?