Review: Cheniere Energy - LNG export major

Cash generative, highly contracted, with advantaged growth, trading at a 13% IRR.

Summary

What it does: liquefies natural gas for export.

Elevator pitch: well-managed and cash generative infrastructure company with contracted cash flows, strong growth at high incremental returns on capital, and a large buyback programme.

Mental model: value.

Valuation and potential returns: DCF suggests 13% IRR to 2030 with relatively low risk.

Exchange: NYSE, ticker LNG

Stock price and market cap: $246, $52bn.

Type of holding: this is one of my trades, at a 1-2% position.

IR website: LNG IR

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

Introduction

Cheniere owns two LNG liquefaction assets in Louisiana and Texas. These complex, multi-billion assets cool natural gas into liquid form so it can be shipped worldwide.

I have owned Cheniere continuously for 10 years and have got the sizing more right than wrong over time. I first bought the stock in the mid $30s in 2016, and then sold quite a bit in the mid $60s in 2018. After a lot of progress in the business I added a little in the high $50s in late 2019, and then I made it a 10% position in the low $30s when markets collapsed in 2020. At that point the stock was trading for 3x distributable cash flow if you looked 18 months forward. I sold most of my stock in 2022 at $120-150, 4-5x the price I’d paid 2 years earlier, making it one of my most personally significant investments ever. I largely missed out on the rally from $150 to $250 in 2024/25, but the big percentage gains had been made by then. Finally, I added at $190 in December 2025, and that position is up 30% in 2.5 months.

My early gains were not without risk. The company was developing two new, highly complex, multibillion LNG facilities, and the potential for cost overruns or other problems was significant. It was also highly levered, so the potential downside was great. However, Cheniere is superbly managed. They have consistently under-promised and over-delivered. Today, Cheniere is a materially de-risked company: it is investment grade, with copious cash flows, strong growth at high returns on incremental capital, and significant buybacks.

Let’s dive in.

Why do we need LNG?

Oil is liquid. This makes it easy to move around. As a result, global oil prices are pretty efficient - once you adjust for quality and transport costs, there is basically one global price of oil.

Natural gas is different. It is, well, a gas. This makes it very hard to ship. You can’t put it on a truck or a ship in its natural state. You can put it down a pipe, but pipes are a bitch. They’re expensive, unpopular, and vulnerable, and there aren’t enough of them. As a result, gas prices vary wildly from place to place. Where there is local oversupply, prices are very low or even negative (where gas is a by-product of drilling for oil and there is no local demand). Where there is local undersupply, prices are much higher. This creates incredible arbitrage potential and has incentivised the development of the LNG market. By cooling gas into its liquid state, you can ship large volumes over long distances fairly efficiently.

Fracking transformed the US from being short gas to being very, very long gas. Gas prices plummeted as a result, creating a huge incentive to export gas. LNG is the only way to do this at scale.

Cheniere’s journey and reinvestment economics

Through the 1990s and the 2000s it was more or less consensus that the US would need to import gas in the future. Cheniere was originally conceived as an LNG import terminal. Once it became clear that fracking was a paradigm shift, Cheniere pivoted to producing LNG for export. Thankfully the sites it owned were perfect, and some of the equipment could be repurposed, but liquefaction plants are huge projects and it took over a decade to achieve production at scale. It was an extremely impressive decade: from scratch, Cheniere built two of the biggest LNG complexes on earth, and they delivered each piece ahead of time and within budget. That’s an incredible achievement and evidences one of the key planks of the investment case: management is exceptional.

Cheniere produces 50-53mtpa today, with projects under construction to get it to 60-63mtpa, projects in advanced planning to get to 71-75mtpa, and potential beyond that to get to 100mtpa. Cheniere has two great advantages when it comes to return on incremental capital deployed:

It is building brownfield, which reduces costs. By expanding current facilities Cheniere can leverage current assets and contractor workforces, and deliver additional capacity at a construction cost to ebitda ratio of 6-7x. By my maths this translates into a 20% free cash flow yield to equity, which for assets that will likely run for 60 years is superb.

Cheniere has been shipping LNG for 10 years and has developed an enviable reputation for reliability. Some customers are prepared to pay a premium for this. Cheniere discussed this on the 4q25 earnings call: they are signing 25-year contracts with world class counterparties with a tolling fee of more than $2.75/mmbtu, when they estimate the market rate is below $2.50. If the spread is 30c, Cheniere are getting 12% more ebitda per $1 of capex than the average.

Cheniere’s business model and commodity sensitivity

Cheniere aims to sell 95% of its production under long term contracts, making its cash flows highly predictable. These contracts are priced to provide Cheniere with a return on its investment. They do not have exposure to commodity prices and tend to be with investment grade counterparties, so I think it is reasonable to view the profits from these contracts as low risk.

The other 5% of production is sold by Cheniere’s marketing arm, CMI, which captures the spread between whatever it can buy gas for in the US and whatever it can sell LNG for overseas. These profits are therefore “at risk”, but the risk skews to the upside because Cheniere doesn’t have to produce these volumes if the spread isn’t attractive. As long as CMI locks in its purchase and sales prices at the same time it can’t lose money, but when global LNG prices spike it can make lots.

One of the counterintuitive outputs of this business model is that in the long term, Cheniere might benefit more from low LNG prices than high ones. Although CMI will makes less money at low LNG prices, Cheniere is primarily in the business of deploying capital into brownfield growth under 20-year contracts at 20% FCF yields on equity. To do more of this, it needs more demand for LNG. And for that, it needs low prices.

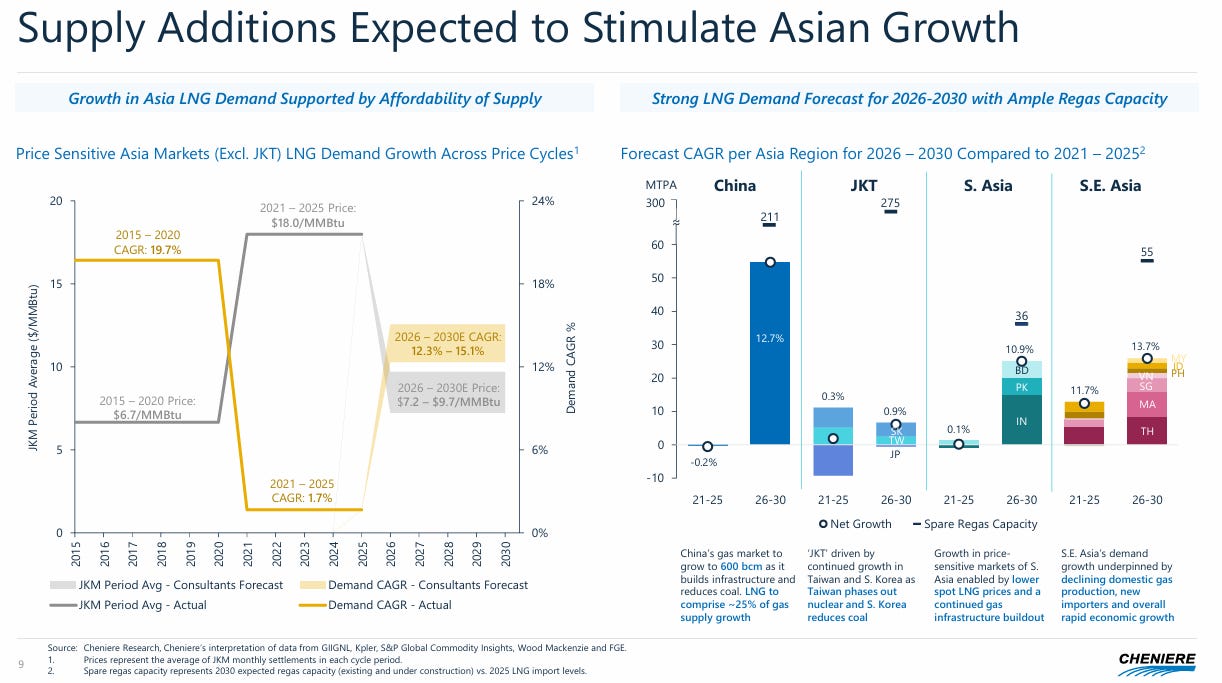

LNG market outlook

The LNG market has had an “interesting” few years. The late 2010s saw a rapid expansion of global supply and rapid demand growth out of Asia as a result. A dearth of projects in the early 2020’s meant less new supply, and there were projections for a tighter market. Then Russia embarked on its appalling invasion of the Ukraine. In response, Europe switched rapidly from buying Russian gas to buying LNG, tightening the market rapidly and pushing global LNG benchmark prices to very unusual levels. In effect, Europe outbid Asia for volume: Asian buyers tend to be price sensitive, so Asian LNG demand has barely grown since 2021.

Over the last couple of years the outlook has shifted again. European demand has become the new normal, and the market has largely adapted to it. A wave of LNG liquefaction projects over the next few years will add significantly to supply. And Asia has continued to invest in regasification and gas distribution capacity, which stands waiting to absorb new supply at lower prices.

To a great degree, this doesn’t affect Cheniere, which has 95% of its production through 2035 already contracted. But it’s worth knowing, because there will be headlines about an LNG supply glut. The tl;dr is: yes there is a lot of supply coming, but it is likely to stimulate Asian demand. Says Cheniere: “we’ve always been of the view that moderate prices are good for this industry.”

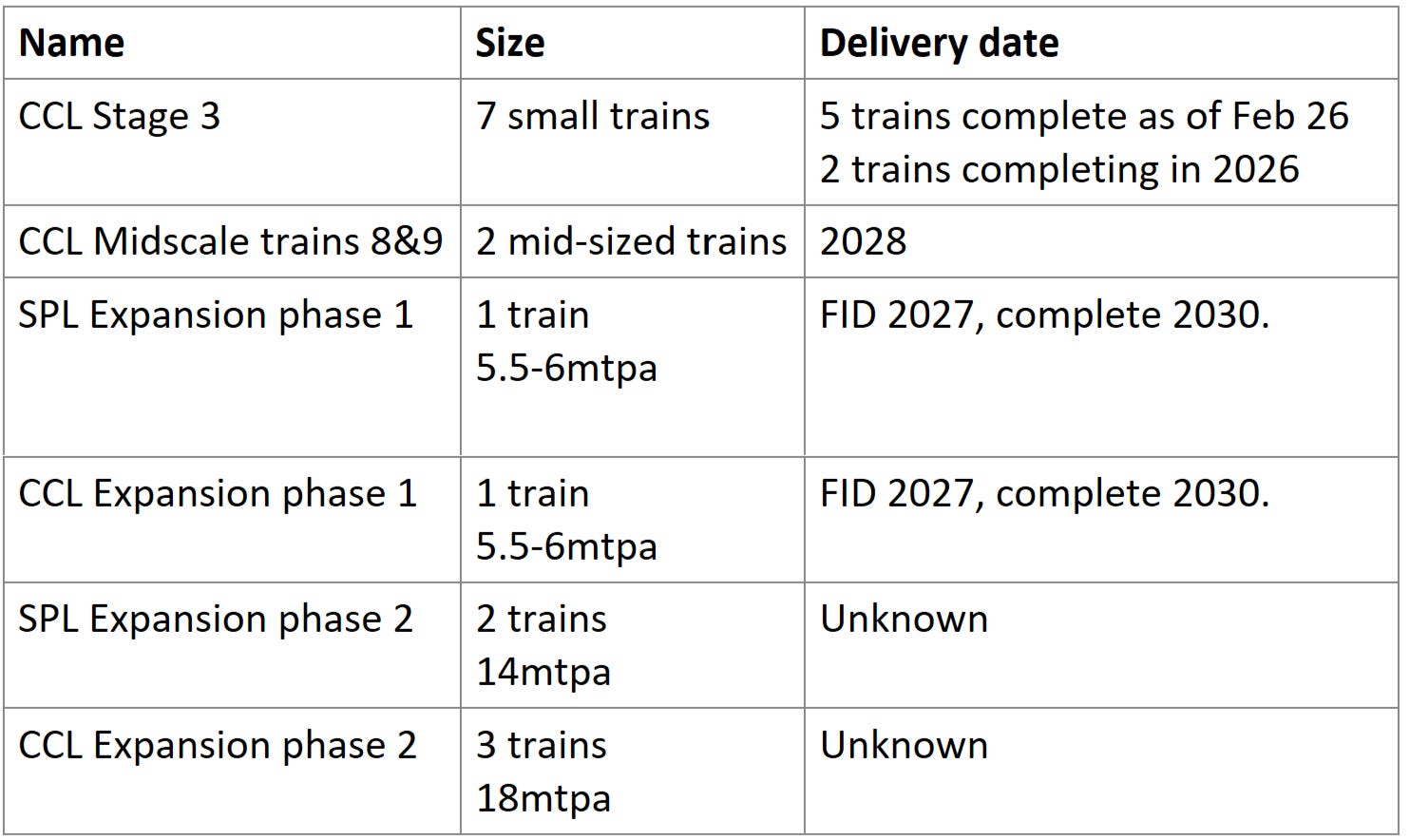

Growth projects

The following projects take Cheniere to 60-63mtpa of production in 2028, and 71-75mtpa in 2030, and 100mtpa thereafter:

Legal & capital structure

Cheniere owns its Corpus Christi asset outright but it owns its Sabine Pass asset through a partnership which is separately listed (CQP). As a result

Cash flow growth is not linearly correlated to production growth - if the growth is at Sabine Pass, Cheniere only owns 51% of it.

You have to adjust for minority interests when calculating an ev/ebitda ratio. The lazy way to do this is to add the part of CQP’s market cap that Cheniere does not own to the EV. This doesn’t help you distinguish between the valuations of Cheniere and CQP, but it is good enough for a sense-check.

As it happens, the majority of Cheniere’s growth is at Corpus. Corpus has 21mtpa of capacity now, with 9mtpa under construction, and potential for 24 beyond that, giving a total of 54mtpa and 33mtpa of growth. Sabine Pass has 30mtpa now, with none under construction and potential for 20mtpa, giving a total of 50mtpa and 20mtpa of growth. This doesn’t affect the economics, but Cheniere owns a higher percentage of the growth at Corpus than at Sabine.

On the capital side, like most infrastructure companies, Cheniere is levered. On a consolidated basis it finished 2025 at 3.3x net debt/ebitda, including operating leases but excluding restricted cash. The debt structure can be seen at page 19 here. The debt is well-laddered, and has been coming down in both absolute and relative (to ebitda and asset) terms. Growth is funded 50/50 equity/debt, which is a very effective way to de-lever in relative terms. Cheniere had 5 ratings upgrades in 2025 and has had many more over the preceding years.

Management

Key to the investment case is the management team. It is incredibly hard to create a business like this from scratch, and to build multiple multibillion-dollar assets ahead of time and underbudget, but this team has done so consistently. They have also communicated with the market consistently and clearly, and they have implemented a highly rational capital allocation plan that has allowed them to:

Grow the business from 0 to 50 mtpa.

De-lever the business, both by paying down debt and by funding ebitda growth with equity, and achieve investment grade.

Reduce the share count from 257m at the peak in 2018 to 210m now, per TIKR.

Management have also had some luck, of the sort nobody wants. Over the last few years Cheniere has grown production fast and ahead of schedule. As a result, the company has had more cargoes to sell at spot than planned, just when spot prices were high because of the war in Ukraine. This has generated excess cash flow which Cheniere has used to de-lever and buy back shares. I hope they do not get that kind of luck again, although as I type LNG prices have spiked on the Iran war.

Risks

Russian gas might come back. I regard this as a low risk; Russian gas production has mostly been redirected to Asia rather than curtailed. If the political situation changes dramatically Europe might start importing more Russian gas, but they have already built LNG regas infrastructure and will remain an opportunistic LNG customer. And in the end, lower prices serve to grow the gas market.

Long term margins. Cheniere aim to sign contracts (and market spot gas) at margins of $2.50-3 per mcf. This has increased from $2-2.50 when they started out, which implies that they have been able to increase margins as the cost of building assets has risen. However, if LNG liquefaction capacity gets overbuilt in the future, margins will come down when contracts begin to roll off. In the worst case, LNG liquefaction might end up like oil refining, which is highly commoditised and done on a spot basis with no long term contracts. I think this is possible, but not soon: as long as buyers need to incentivise new capacity, long term contracts will be needed. I see this as a 2050 risk.

Feedgas. Cheniere is basically built on the shale revolution. That’s what supplies the gas that Cheniere cools and sells. It is clear that the rapid growth phase of North American shale is over. That in itself is not a huge problem: there is plenty of gas and it remains cheap by global standards. However, some analysts such as Goehring & Rozencwajg argue that gas production will now enter a long decline. That might well make Cheniere’s product uncompetitive, pressuring margins once contracts start to roll off. I think G&R get a lot right, but I think their argument is more compelling at $50 oil and $2 gas than it is at $65 oil and $3.50 gas. Said another way, I don’t think it takes a huge uplift in the gas price to incentivise more drilling, and I don’t think the shales are so exhausted that drilling won’t work.

Hurricanes. Cheniere’s assets are on the Louisiana and Texas coasts, potentially in the direct path of a hurricane. However management have known this since day 1. The assets are built to withstand hurricanes, and procedures are in place.

Impact of the Iran war

If the war escalates and Qatari LNG exports are impaired in any serious way, LNG prices could stay high. This benefits Cheniere but not transformatively since most of its volumes are contracted (and most of what isn’t contracted has already been forward sold for 2026).

Equally, if the war ends tomorrow, Cheniere might immediately trade back to the low $230s, where it was prewar.

In short, I don’t think the war is hugely relevant to Cheniere unless it escalates and lasts for a long time. I very much hope that is not the case but if it is, Cheniere will benefit from being a reliable supplier well away from the war zone.

Valuation

These are long lived assets. LNG facilities can easily run for 50 years and I think well maintained ones with consistent feed gas in a mature market can likely last significantly longer.

Cheniere uses a bespoke metric called distributable cash flow, or DCF. This is basically ebitda less maintenance capex, interest, and cash tax. It overstates long term owner earnings in 2 ways: first, these are new assets so maintenance capex is fairly low; second, Cheniere is still investing hard which creates tax allowances. However DCF is an accurate measure of the cash the company will produce over the next 5-10 years, so I think it is a reasonable valuation tool. Cheniere’s latest DCF guidance is laid out on page 13 here.

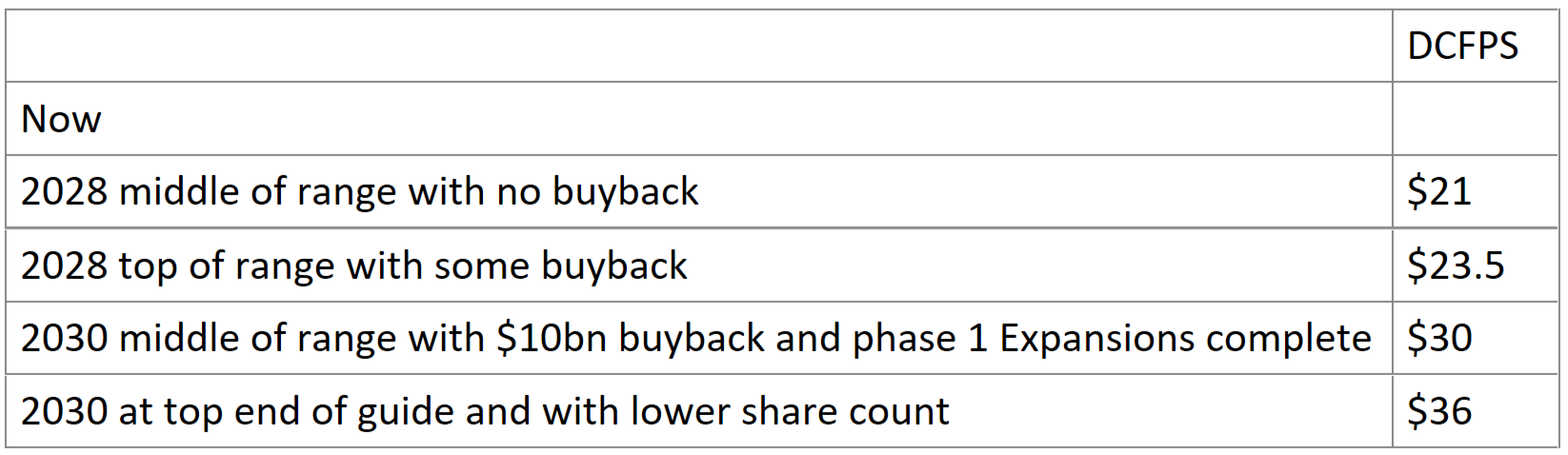

Once projects currently under construction are completed in 2028, the company will produce 60-63mtpa and $21 of DCFPS assuming the middle of the DCF guidance range and no further buybacks. However, management consistently beats guidance and they are buying back shares. Assuming the top end of the guidance range and a share count of 200m, 2028 run rate DCFPS reaches $23.5.

Once the company has completed its $10bn authorised buyback and the CC and SPL Expansion projects, all due by 2030, DCFPS guidance increases to $30. I think they will beat this. Again, guidance uses the middle of the range for DCF but tend to beat guidance, so I think we can use the top end. Also, I don’t think they have accounted for all of their FCF. On the 2q25 call the company guided to $25bn of DCF from 2h25 to 2030, and $7.5bn of equity investment to get to 71-75mtpa of production in 2030. Of this, $2.4bn of DCF was to be produced and $1.4bn of capex was invested in 2h25, leaving $22.6bn of DCF and $6.1bn of capex for 2026-2030. This nets to $16.5bn of FCF over those 5 years. The dividend will consume ~$2.5bn leaving $14bn. Guidance assumes a $10bn buyback, leaving $4bn unaccounted for. Either the buyback will be bigger than guided, or the company will keep growing production.

Finally, the 2030 guidance assumes $10bn of buybacks at $285 per share. This is well above the current share price, which is a sensible assumption for a management team issuing guidance. However as an investor I’m equally interested in how many shares the company could buy back at the current price. If all FCF (after dividends) is used to buy back shares at the current price the 2030 share count will be 157m, not the 175m that management assume. With that share count, and using the top end of the DCF range, we get nearly $36 in DCFPS.

To summarise:

The implied multiples seem reasonable to me for a long-lived, highly contracted, cash-generative asset. I also run a simple DCF which assumes that all FCF after dividends is used for buybacks at the current price, and at the end of 2030 the stock is valued at 12x 2031 DCFPS, which seems fair given they will still have a runway for 33% growth (75mtpa to 100mtpa) at advantaged economics.

With a DCF built this way, the IRR is doubly sensitive to the share price because it affects both the starting point and the buyback. The alternative is to guess what price the buyback will average. I like my method because it tells me the IRR if the shares remain at the current price, but it is a matter of preference.

My DCF puts the 5-year IRR at today’s share price of $246 at 13%. At $230, the IRR is 15%; at $290 it is 8%. For me, it is a comfortable hold at the current price.

Links to previous work

If you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete