Review: Helios Fairfax Partners - Africa at a discount

Diversified exposure to private African equities with a free option on the asset manager.

Summary

What it does: invests and manages third party investments in Africa.

Elevator pitch: HFP trades at a 50% discount to tangible book value. This is too cheap for a diversified collection of interesting African opportunities plus exposure to the fee streams from managing third party capital. Exposure to the emerging markets fundraising cycle, which is at a 10-year low, is an added bonus.

Mental model: value, potential scaler (read about my mental models here).

Valuation and potential returns: 50% of TBV allows for potential returns of 15-30%.

Exchange and ticker: TSX, HFPC.U

Stock price and market cap: $1.70, $190m.

Do I own it? Yes.

IR website: here.

Tag for finding my other articles on this stock: HFP

About this blog: I have been investing for 25 years, professionally and personally. I look for stocks that have a high probability of compounding at 15% for at least 5 years with limited downside. I write these stocks up on my blog. You can find more about me, my philosophy, my mental models, and my portfolio structure on my site.

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

Introduction

Helios Fairfax Partners (HFP) is the product of the merger of Helios and Fairfax Africa Holdings - one a leading alternative asset manager, the other a permanent capital vehicle, both focused on Africa. The company combines alternative asset manager fee earnings and carry with permanent capital for investing in some of the youngest, fastest-growing, and capital-constrained economies on earth. As a result of liquidating legacy investments and a downcycle in emerging market fundraising, the stock screens poorly and trades at less than half of book value. But book value has now grown for 5 quarters in a row, newer investments seem to be performing, and the asset manager fee stream may be turning a corner. The company aims to compound book value at 15% and pay asset management profits out as dividends. If it can do this, the returns from today’s discounted price will be excellent.

History

In 2004, Tope Lawani and Babatunde Soyoye founded Helios as an African private equity fund manager. Helios raised its first African PE fund in 2006, and followed this with larger funds in 2009 and 2015.

In 2017, Fairfax Financial Holdings (FFH) launched a permanent capital vehicle for investing in Africa called Fairfax Africa Holdings (FAH). It didn’t work and by 2020 FAH was looking for strategic alternatives. They landed on the idea of merging with Helios. Helios got a permanent capital vehicle and FAH got a share of Helios’ economics.

This looked great on paper but the period from 2020-2024 was a nightmare. Helios liquidated the old FAH portfolio as best they could, but took losses along the way. In addition, covid and its consequences (inflation and rising rates) made it hard to exit investments in legacy Helios funds and raise funds for new ones, meaning significant amounts of carry was lost and management fees went down. Book value per share (BVPS) fell for 7 years in a row, so HFP screens horribly.

However, under the surface, progress was made. By 2024/5 pretty much all of the legacy portfolio had been sold and reinvested in much more promising businesses. And while emerging markets fundraising is still in a downcycle, that cycle will turn, and investments in the fundraising team and in diversifying the product offering show early signs of bearing fruit.

Alignment

FFH owns 30m multiple voting shares and 7.3m subordinate voting shares. That gives them a 35% economic interest and a 53% voting interest. Principal Holdco, which is owned by Lawani and Soyoye, owns 25.5m multiple voters and 24.6m subordinate voters representing a 46% voting and economic interest. The remaining subordinate voters trade on the TSX. These are what we can buy; they represent 19% of the economic interest and virtually no voting power.

Some will view the lack of voting power as a red flag. I don’t, for at least three reasons.

Having controlling shareholders focused on the long term prevents shareholders doing something value-destructive for short term gains (such as winding up the company when it trades at a big discount).

I think having management with skin in the game is more important than having voting control - especially in alternative asset management. Lawani and Soyoye both have the substantial majority of their net worth in HFP stock, per AGM Q&A.

Fairfax has voting control, which creates a balance of power.

Why Africa

Africa has incredible potential, and a reputation for squandering it. This reputation is deserved, but progress is being made. African countries account for 12 of the 20 fastest growing countries in the world in 2025-6. Over the next few decades Africa should be transformed. The investment case is underpinned by robust growth, a rising working-age population, rapid urbanisation, and improving business environments, despite enduring infrastructure and governance gaps.

HFP targets two megatrends. The first is demographics and urbanisation. Africa is staggeringly young, with a median age of about 20. Its working-age population is growing around 3% a year: by 2035 it will be bigger than China’s; by 2050 it will have doubled; and in 2100 Africa will be the only region on earth that has a bigger working-age population than today. In addition, Africa is urbanising. In 2009 Africa had 52 cities with 1m people or more; today, it has over 100; by 2050 it will have 160. The total urban population will double by 2050. This matters economically: urban populations are dramatically more productive than rural ones. Every urban resident needs housing, transport, healthcare, education, food retail, financial services, and connectivity. Urban consumption is also fundamentally different from rural subsistence: it is monetised, formal, and financeable. Africa is creating a large consumer class in economies that remain extraordinarily underserved.

HFP’s second megatrend is technology and innovation. Africa is poor and suffers chronic infrastructure deficits. As a result, customer value is low and the cost to serve is high. In addition Africa has cheap labour but a very high cost of production when you take skills gaps and logistics costs into account. Technology and innovation help solve these problems. Africa is leapfrogging expensive legacy technologies - mobile phones and internet rather than landlines and broadband, household solar rather than vast power generation and transmission networks, e-banking rather than inefficient branches, online skills development rather than poor government schools. Mobile money, pioneered in Kenya with M-PESA and now ubiquitous across East and West Africa, has given hundreds of millions of African adults access to formal financial services for the first time with just a basic mobile phone. And if exports are increasingly digital, Africa’s lack of physical infrastructure will be less important. Helios: “the good thing is that [in just the last 7-10 years] more and more young people are getting into technology and building platforms and coming up with great ideas.” Technology is both driving growth by solving inefficiencies and creating great investment opportunities.

The pushback is governance. Africa is poorly governed. Institutions are weak, economies are overregulated, currencies are unstable. But remember:

Africa is diverse. There are 54 countries, and some are much better than others.

Helios invest in companies, not countries. Companies with reliable counterparties, hard currency revenues, and exposure to multiple countries are more resilient than others.

Things are improving. This is important: money is made when things go from bad to ok. What are the signs of progress? Here are two: a growing number of countries in Africa have regular elections and peaceful transitions of power, and the World Bank says that Sub-Saharan Africa undertook more business environment reforms than any other region from 2010-2020. (Rwanda rose from near the bottom of the Ease of Doing Business ranking to the top 30 over 15 years via a systematic programme of regulatory simplification, e-government, and anti-corruption enforcement, and a landmark long term initiative is the African Continental Free Trade Area, which aims to eliminate intra-Africa tariffs on most goods and services and eventually create a $3.4tn African single market.)

One of Helios’ most successful investments was a telecom tower business in one of Africa’s worst-governed countries, the Democratic Republic of the Congo.

I do not count Africa’s abundance of natural resources as an advantage. In areas with poor governance, natural resources are a curse, encouraging corruption and driving boom-bust cycles. One possible exception is agriculture, which is labour intensive and hard to monopolise, so compared with (say) mining it is better for people and less tempting for corrupt politicians. Africa is blessed with an abundance of farmland and cheap labour. Slowly, slowly it will build the infrastructure to exploit these advantages.

Because Africa’s GDP is tiny and its governance is poor, it receives very little investment. Even compared to other emerging markets there are massive funding gaps for venture capital and private equity. As a result, valuations are low. This will slowly change. As GDP rises, inflation comes under control, currencies stabilise, and local savings grow, financial markets will deepen. This trend has been clear in Latin America over the last 40 years and I think it will happen in Africa over the next 40.

The point of this section is not to persuade you that Africa is the next China. It isn’t. But it has compounded GDP at 4-5% since the late 1990s and I see no reason why it cannot keep that up. If it can, then the living conditions of 2 billion people will be absolutely transformed. Africa’s GDP per capita is $2,000, or $7,000 in purchasing power parity terms. That is roughly the threshold between subsistence and the emerging middle class. In other words, the next decade or two of growth will see more and more Africans able to buy aspirational goods, pay for healthcare, save for the future, and spend on experiences. Nascent markets will become vast and significant companies will be built.

Balance sheet

HFP’s balance sheet splits into 3 broad categories:

Investments in the Helios funds.

Co-investments alongside the Helios funds.

Helios, the asset manager, which is now consolidated on the balance sheet (appearing in various line items) but appears in the investment list as TopCo.

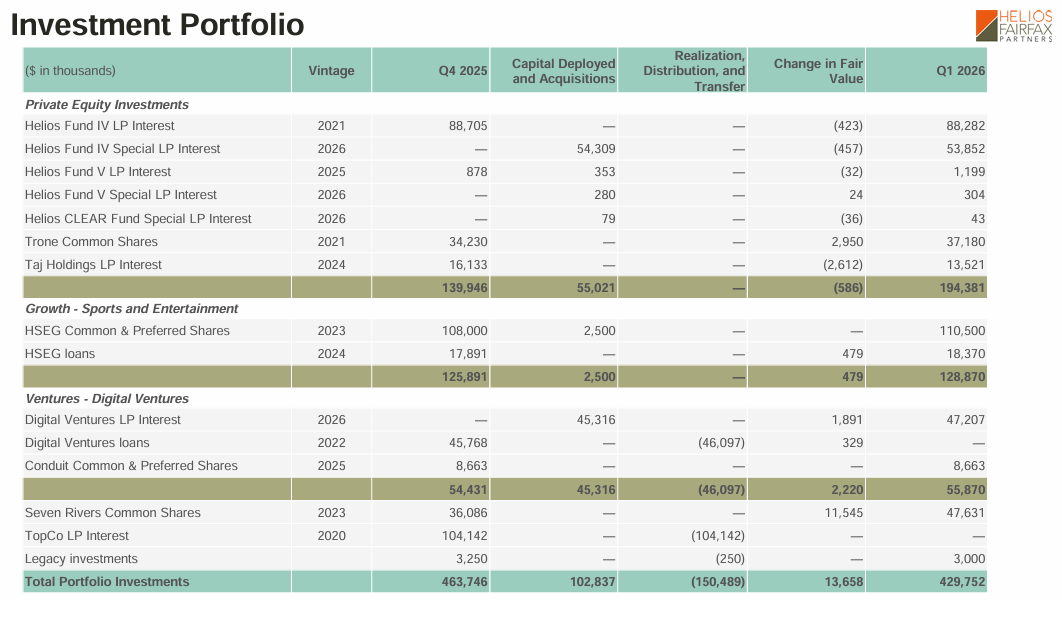

Funds and co-investments

Before we dive in, a word on valuations. The funds are carried at NAV. There isn’t much disclosure on the valuation of the assets inside the funds, which is irritating. We do know that several assets are valued using comparable market multiples, which is arguably less open to manipulation than a DCF but introduces some volatility. Two things give me some confidence: several of the funds (or their successors) are raising capital, which suggests third party investors find the valuations palatable; and where valuations are disclosed, which is mainly for the co-investments, they seem reasonable.

Helios IV and V are Helios’ latest private equity funds. The LP (Limited Partner) interests arise because HFP seeds the funds to help attract third party capital. The SLP (Special Limited Partner) interests arise because, like most managers, Helios makes a GP commitment to its funds which it calls the Management Team Commitment. HFP funds 50% of this commitment (the SLP interests) in return for 50% of any carry earned. Unless FFH agrees an exception, HFP’s SLP contributions are capped at the lesser of $7.5m per fund or 2% of aggregate fund. Neither HFP’s LP nor SLP Interests incur management fees or carry.

Substantially all of HFP’s PE exposure ($142m) is to Helios IV, which will mature over the next few years. Its IRR through December 2025 was 23%. That is unrealised, but promising: HFP’s investment has doubled on the back of strong investee company performance. HFP lists 7 private companies held by Helios IV in payments, insurance, discount grocery retail, healthcare, and data centres.

Helios CLEAR (Climate, Energy Access & Resilience) targets climate adaptation and mitigation investments in Africa. It has raised $250m and is seeking more. It made its first investment in 2025. HFP’s investment in CLEAR is small but it is significant because it represents a new fund family.

Helios Sport and Entertainment Group (HSEG) is a private permanent capital vehicle which HFP seeded by contributing cash, loans, and its NBA Africa stake. HFP’s current exposure is $18m in loans and $111m equity, which is up from $87m at cost. In 1q26 HSEG achieved a first $30m close on a $75m Series B round, of which $28m was third party capital. Africa has vast talent and global success in sport, music, and content generally. HSEG invests in sports rights, content, and ecosystem enablers like NBA Africa, venue management companies, and talent agencies. All of these attract large scale, blue-chip capital in other geographies - but not in Africa, where HSEG has something of a first mover advantage.

HSEG’s marquee asset is its holding in NBA Africa. Africa has exported players to the NBA for decades, and as a result basketball is the second most popular sport on the continent (after football) despite approximately zero investment. Interestingly, and in contrast to football, in some countries 40% of the fan base is female. Historically, an investment like this would have been difficult to monetise in Africa, where most people can’t access or afford all-you-can eat cable subscriptions. However with the advent of smartphones content can be monetised in new ways - for example pay per view, highlights only, or with discounts for watching a day late. I really like the fact that HFP can make potentially multi-decade investments like this because it has permanent capital. NBA Africa was not prepared to transact with a time-limited fund.

HSEG’s other investments are the African part of the Professional Fighters League, which is the second largest MMA business globally after UFC; Zaria, which was cofounded by Masai Ujiri and builds marquee sports and entertainment arenas in mixed use developments such as Zaria Court in Kigali and Nairobi’s Railway City (overview at 16:30 but the whole video is interesting); and The Malachite Group, which organises music festivals and events and manages African talent. Several of these investments are loans with equity-like upside.

Helios Digital Ventures (HDV) targets early stage tech companies with potentially exponential outcomes. HDV aims to invest $5-20m in rounds of $20-50m to build pan-African tech businesses of the kind that have emerged in Asia and Latam. It has invested in payments, fintech, biotech, and SAAS. HFP’s stake started as an accruing loan. At yearend 2025 this was converted into an LP interest and in 1q26, its first quarter as equity, the stake was marked up 4% to $47m.

Seven Rivers was a hedge fund investing in public equity and credit in Africa. Its performance seemed strong - 50% in 2025 and another 30% in 1aq26 - but the decision was taken to close it in April 2026. The $48m stake will therefore be liquidated and added to the $14m in cash on hand.

Co-investments. HFP invests in individual companies when the holding period is likely to be very long and/or when it wants additional exposure to a specific idea. Current direct holdings are:

$37m in Trone, which distributes and maintains medical imaging and diagnostic equipment and produces and distributes contrast pharmaceuticals for imaging in Morocco and Francophone Africa. HFP has additional indirect exposure through Helios IV - between them, Helios entities and the management team own the whole company. HFP is up 140% on its investment, which is carried at 9.4x ebitda.

$14m in Taj Holdings, which owns HFP’s direct stake in M2P, an Indian infrastructure API and Banking-as-a-Service provider rapidly expanding across Africa. HFP has additional indirect exposure through Helios IV. The stake is valued at 6.8x revenue and has been marked down from $16m at cost on lower market multiples and lower forecast revenue. HFP has a liquidation preference.

$9m in Conduit, which is building stablecoin-based B2B cross-border payment infrastructure for emerging markets in Latin America and Africa. HFP has additional exposure though HDV, which invested in 2023, 2024, and again in May 2025 when it participated in a $36m Series A led by Dragonfly and Altos Ventures. HFP then added its direct stake in November 2025 (although NB I think there are multiple share classes with different exposures). The latest operating data I have is that transaction volumes grew 16x in 2024 to an annualised rate of $10bn.

Pending: up to $75m in CAB Payments. Over the last few months there has been a tussle for control of this company, a London-listed cross-border payments and banking provider. Helios IV has owned 45% since before the IPO. Following share price weakness HFP and Helios V have jointly offered to buy the remainder. StoneX have bid a similar price, which goes some way to validating the valuation, but abandoned their offer because Helios IV did not support it. The bid has over 50% voting support, but the board has rejected it as too cheap. If it closes, it will obviously be significant for HFP.

Helios

Asset management is a great business model - at scale. The infrastructure required to gather and invest capital, once built, can generally support growth without too much additional cost. This operating leverage drives high margins and economies of scale. Unfortunately Helios is subscale - but that’s why you don’t have to pay for it. It is, in effect, an option.

Helios raises capital, invests it, and charges management and carry (performance fees). For its core funds, the management fee is typically 1.5-2% and the carry is 20% of profits over an 8% compounded hurdle. HFP, through TopCo, gets:

Any excess of management fee revenues over operating costs - i.e., any profits (although Helios is currently lossmaking).

50% of any carry (the remaining 50% goes to the Helios team, which encourages long term thinking and employee retention since it usually takes years to earn carry).

On paper HFP pays Helios a fee for investing its balance sheet, but this is eliminated on consolidation. What shows up on the HFP income statement is just third party fees less the cost of running Helios. This is actually a good representation of the real economics: the fee is irrelevant; what matters is that HFP covers Helios’ losses. This subsidy represents the cost of sourcing investments for HFP and the cost of maintaining its equity option in Helios. Based on the 1q26 P&L, the annual cost is 2.3% of HFP’s tangible book value (TBV). Given the value of the option I think this is a good deal: Helios will be very valuable if it can raise more third party capital and turn consistently profitable.

Can it?

Helios was founded in 2004 and raised a succession of funds in its core PE strategy: Helios I at $300m in 2006, Helios II at $900m in 2009, and Helios III at $1.1bn in 2014. Performance was decent, and by 2019 Helios anticipated receiving significant amounts of carry. However after 2015 the emerging markets fundraising cycle turned down, and then covid hit, depressing business activity, hurting valuations, and slowing exits. This impacted Helios in two ways. First, the anticipated carry evaporated as valuations came down, time dragged on, and the 8% hurdle compounded. And second, the fundraising environment became almost impossible so Helios IV, raised in 2020 at $355m, was only one-third the size of Helios III. What looked like a steady fee grower with carry on top hit a nasty bump in the road.

That bump may now be in the rear-view mirror. Helios IV’s performance has been excellent so far. That’s good for carry and great for fundraising. Helios V’s first close was $338m, almost as big as the whole of Helios IV. Its target is $750m, which would be a significant step back towards the scale of funds II and III. In addition Helios has attracted third party capital into two new strategies: CLEAR 1 is the first of a new fund family and has raised $250m out of a targeted $400m, while HSEG is a permanent capital vehicle which has raised $30m out of a targeted initial $70m.

In 1q26, HFP consolidated Helios for the first time. Historically it carried Helios (TopCo) on the balance sheet at DCF fair value and changes in fair value went through the P&L. There was almost no disclosure of Helios’ actual economics. Now, Helios’ fee streams and costs are reported on the P&L, making analysis much easier. We only have figures for 1q26 but the key numbers were management fees £5.9m, consulting fees $2.9m, and G&A $10.8m, for fee-related earnings of -$2m in the quarter and -$8m annualised. (As discussed above, this loss equates to 2.3% of TBV.)

I think these losses will improve over time, but not necessarily in a straight line. Helios’ major fee generators are currently Helios IV, V, and CLEAR 1. These funds earn fees over committed capital. This means each fund generates flat fees for several years and then declining fees as investments get sold. Helios II and III stopped paying fees in 1q26, which could lead to a drop in fees in 2q26 although the disclosures aren’t clear. Helios IV should start selling investments over the next few years. Helios V and CLEAR 1 will need to raise additional capital to offset these factors. In short: differences in timing could drive quarterly volatility in fee related earnings but investors should look through this. It is the trend that matters.

Helios’ other important profit stream is carry. Helios’ performance record is respectable. In total, funds I, II, and III raised $2.3bn. They have so far generated $4.7bn via exits (2026 AGM transcript) but little carry - carry is calculated over an 8% compounding hurdle so it is very sensitive to exit timing, and covid delayed caused delays. Helios IV looks more promising. It has produced an unrealised IRR of 23% so far, and HFP’s share of its unrealised carry stood at $22m as of yearend 2025.

While we are on the topic of performance, two points are worthy of note. First, Helios uses less leverage than US PE: in 2023, >20% of all US PE deals had >10x debt-to-EBITDA and ~60% had >6x. For Helios, leverage is typically less than 30% of the capital in a deal. Second, Helios’ exits are high quality. Most of the $4.7bn of exits from Helios I, II and III to date were IPOs or sales to strategic buyers, not pass-the-parcel amongst financial owners.

Two final things could help Helios grow:

A turn in the emerging markets fundraising cycle. EM was “hot” through the late 2000’s and early 2010s, on the back of rapid GDP growth, strong currencies, and high commodity prices, all of which tend to be correlated in EM, plus a lack of investor enthusiasm for investing in the developed world after the GFC and the Eurozone crisis. This dynamic aggressively reversed after 2015 and EM funds have found it extraordinarily hard to raise money for a decade. But this is a cycle, and it will turn. I actively seek exposure to this.

Successfully launching a fourth major strategy (after PE, CLEAR, and HSEG). Seven Rivers had good performance but did not attract third party capital and has been closed. Helios Energy Transition Infrastructure (HETI) was going to be a public vehicle investing in long dated, dollar + inflation infrastructure assets, but was shelved in 2024. Either could be resurrected if conditions change. Digital Ventures is nascent but ongoing. Helios DataSphere is in development as a pan-African data-centre development and operating platform. HFP’s balance sheet is an advantage here because Helios can seed funds without third party capital. It is far too early to ascribe value to the fees new strategies might generate, but it is positive that Helios is trying to diversify its fee streams.

Putting this together, it is quite possible that by around 2030 Helios could have:

Two recurring fund families (PE and CLEAR) capable of raising funds in the +/- $1bn range.

A growing permanent capital vehicle in HSEG which I guess might have $2-300m of third party capital.

Small but growing third party assets in a fourth major strategy.

Realised carry income from Helios IV.

Unrealised carry building up from Helios V and CLEAR I.

An EM fundraising cycle turning in its favour.

Almost any combination of these things would make Helios a very different animal - bigger, more profitable, and more diversified than it has ever been.

Other balance sheet notes

Total liabilities are 23% of tangible assets and borrowings are 7% of tangible assets.

HFP has $33m in debt including a small amount of fund level leverage which is secured on fund assets but ultimately is recourse to HFP.

HFP has drawn $10m of a $100m facility maturing Feb 2031, at SOFR + 6%. Including $14m in cash and $48m in Seven Rivers which is being liquidated, HFP has significant liquidity.

Borrowings would be 22% of tangible assets if HFP maxed out its loan facility and invested the proceeds in tangible assets.

HFP has unrecognised deferred tax assets ($41 million at year-end 2025), mostly from net capital losses and investment differences.

Limited partner distributions payable is money owed to fund II and III LPs as they wind down.

100% of the SLP Interests is consolidated onto balance sheet and the 50% that is funded by management appears as an offsetting liability (amounts attributable to other limited partners).

Until 1q26, HFP carried its interest in Helios at fair value using a DCF. In 1q26, HFP determined that it should consolidate Helios. No consideration was exchanged but for accounting purposes HFP “bought” Helios at the yearend 2025 carrying value. The DCF inputs for this were disclosed. For management fees, they were 9% growth for 7 years, 4.5% thereafter, 34% pretax profit margins, and a 17% discount rate. For carry, they were exit multiples of 1.5-3.7x, exit dates from 2026-2031, and discount rates of 24-28%. This transaction created $52m of identified intangibles (the present value of expected profits from existing management contracts, of which $2m was amortised in 1q26) and $60m of goodwill (the present value of expected profits from future management contracts, which is subject to impairment testing).

Valuation and expected returns

The share price is bouncing around $1.70. This is a 50% discount to TBVPS of $3.26. TBV is made up of holdings in the Helios funds, direct holdings in African companies, and cash. It does not include anything for Helios, the asset manager. What little disclosure we have suggests carrying values are reasonable, as does third party investor validation. HFP’s balance sheet is only lightly levered, limiting downside. On a balance of probabilities, I am prepared to trust that HFP could realise tangible book value in an orderly liquidation and that TBV will grow as the investments perform.

The discount to BVPS ($4.27) is even greater at 60%. The difference between TBV and BV is the intangibles and goodwill created when HFP consolidated Helios (see above). While I think the assumptions underlying the “acquisition price” are aggressive, they are not insane, and it is interesting that $0.46 per share of identified intangibles represent the expected profits from existing contracts. If you include this the “adjusted TBVPS” is $3.72 and the discount is 54%.

With such large discounts, you don’t need heroic assumptions:

If TBVPS can compound at 10% and the discount moves to 30% over 5 years, the stock could return 17% per year. This requires the underlying investments to do ok, but does not require Helios to work.

If BVPS can compound at 15% and HFP can pay a dividend from Helios profits (which are the goals stated at the 2026 AGM), I would expect the stock to trade at 1x book value in 5 years and it could return 38% per year plus dividends.

Obviously worse scenarios are imaginable. Worse scenarios are always imaginable. But HFP is a diverse collection of carefully-chosen assets in a fast growing, capital starved part of the world. I think an outcome within the range of returns shown above is realistic.

Conclusion

HFP is a diverse collection of seemingly decent investments trading at an extreme discount. It has optionality in Helios, which appears to be heading in the right direction, and also in the underlying investments, some of which could be home runs. It is run by motivated, experienced, and aligned managers. It offers exposure to a turn in the EM fundraising cycle, which I actively seek. It is illiquid, so if interest picks up the stock could move quickly. It is starting to screen better - book value has grown for the last 5 quarters, and its recent consolidation of Helios opens the door to industry-standard valuation metrics. It is one of the more speculative holdings in my portfolio, and one of the smaller ones. But I think it has the potential to deliver excellent returns.

Links to previous Reviews

Thanks for reading - if you enjoyed reading this please subscribe, like, and restack, and do get in touch if you have questions.

Pete