Review: Howard Hughes Holdings - Ackman's Berkshire?

Long term cash flows and practically infinite reinvestment runway - will it work?

Summary

What it does: real estate company becoming a diversified holding company.

Elevator pitch: very long term real estate assets are starting to generate cash. One of this generation’s great investors is deploying it. This combination might make a unique compounding vehicle.

Mental model: moat, value (read about my mental models here).

Valuation and potential returns: potential 3x in 5 years.

Exchange and ticker: NYSE, HHH.

Stock price and market cap: $63, $3.8bn.

Do I own it? Yes.

IR website: here.

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

Introduction and: why now?

Howard Hughes stock has gone absolutely nowhere for 15 years. Why should the next 15 be any different? The answer is simple. The company is starting to generate quite a lot of cash, and will likely do so for decades, and they’ve come up with a very interesting way to reinvest it.

HHH’s core business is in real estate - specifically, Master Planned Communities (MPCs). These assets often take 50-60 years to build out. They consume cash initially but as revenues rise and investment falls they pass a cash flow tipping point. HHH’s MPC business is past the tipping point and is starting to generate significant amounts of cash: I estimate about 50% of the $5.6bn GAV (gross asset value) will be sold within 10 years and 80% within 20 years. The problem is, there are only a few good MPCs nationally, so reinvesting cash into new MPCs can only be done opportunistically - it’s not a strategy.

So what to do with the cash? The obvious answer would be opportunistic buybacks and dividends, with the balance between the two determined by how fully valued the stock is. And right now that would be a good answer, because management insists the stock is undervalued. But it’s not a great long term strategy: eventually the stock will be fully valued, and while dividends return value to shareholders, they don’t create it.

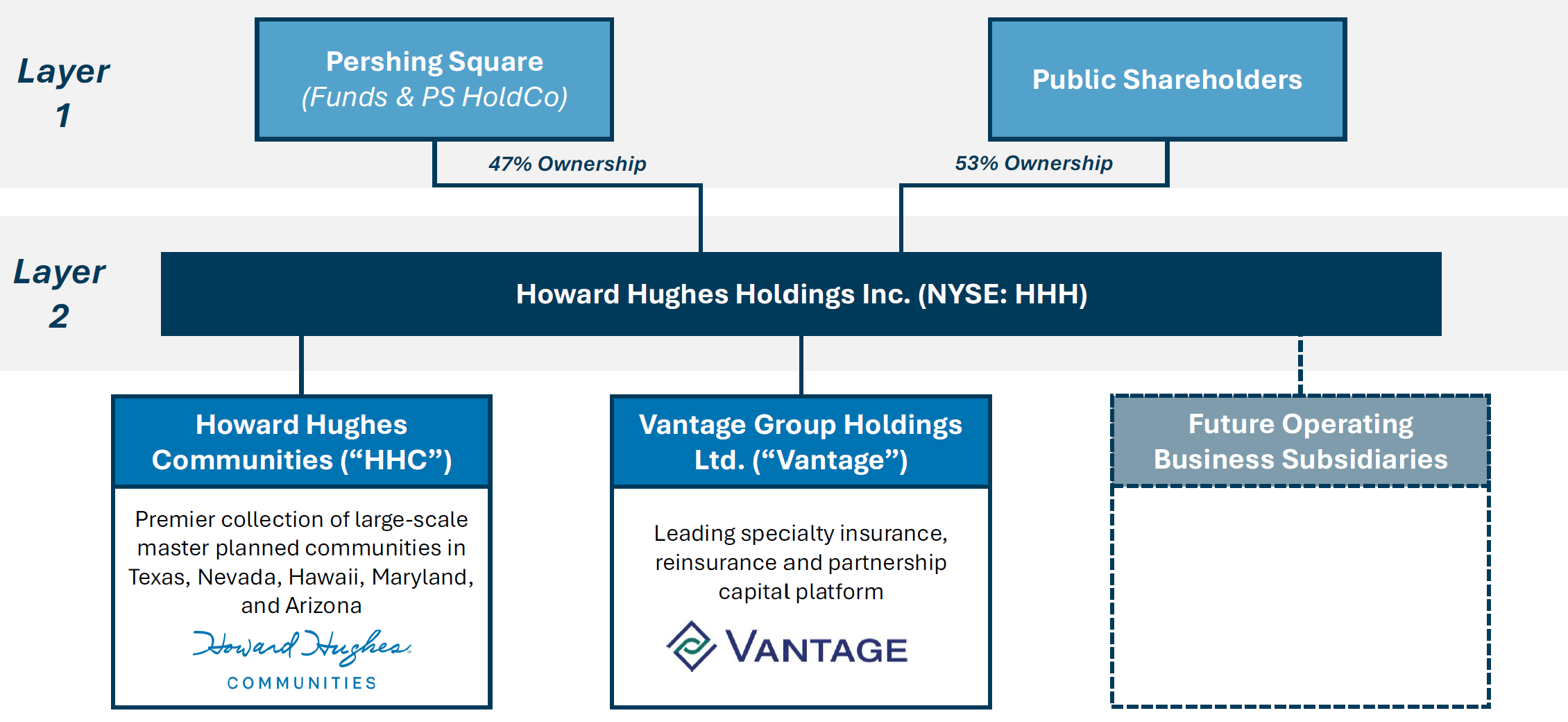

Enter Bill Ackman’s Pershing Square Capital Management. Pershing has been involved with HHH for years, and in 2025, HHH hired Pershing Square to build a diversified holding company. This is riskier than the buybacks and dividends strategy, but if done well will create more value, because it means HHH has a very long reinvestment runway. It can now invest its cash into:

Buying a portfolio of minority stakes in listed companies for value. This runway is not all that long if it is done on HHH’s balance sheet - eventually they’d be classified as an investment holding company, which would bring a regulatory burden they don’t want. However by buying an insurance company and putting the minority positions onto the insureco balance sheet, HHH can redeploy any amount of MPC profits into this portfolio.

Buying control positions in private businesses.

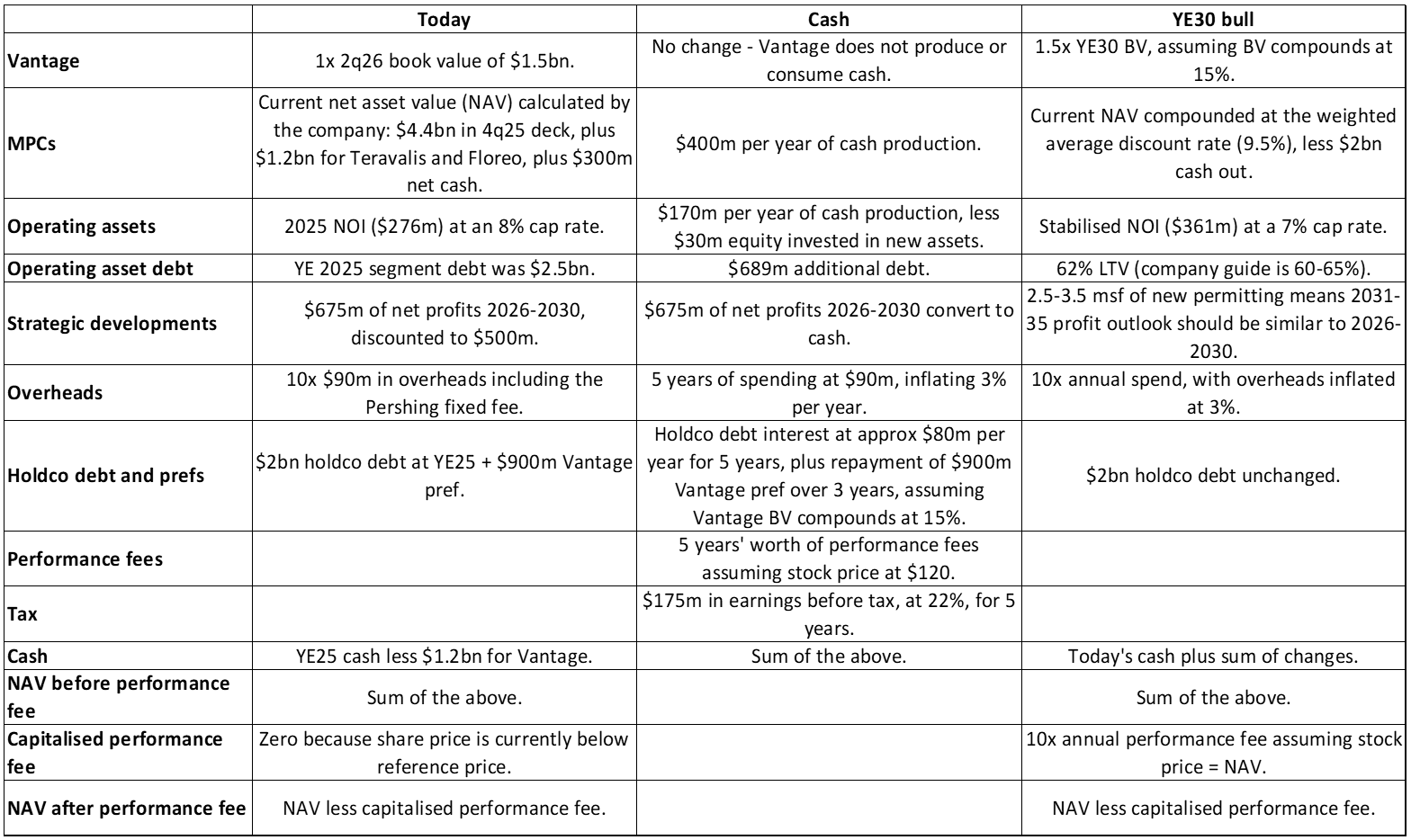

As part of the deal, PSCM injected $900m of new capital into HHH by purchasing common stock at $100 per share. This cash will help fund the acquisition of Vantage, an insurance company. The balance of the investment will be funded by Vantage preferred stock issued to Pershing Square Holdings (PSH). Vantage’s shareholder equity will be invested into a portfolio of common stocks similar to Pershing’s existing portfolios. Future MPC cash flows will be used to pay down the Vantage prefs, and once that is done they will be invested into either control positions in high-quality private businesses or into additional insurance company equity (and therefore listed stocks), depending on where the best opportunities are. The structure looks like this:

This strategy looks incredible on paper, and might actually work. Pershing Square’s investing credentials are clear. But it will not be easy: a lot comes down to Pershing Square’s execution, and whether they are worth their fat fee.

Valuation

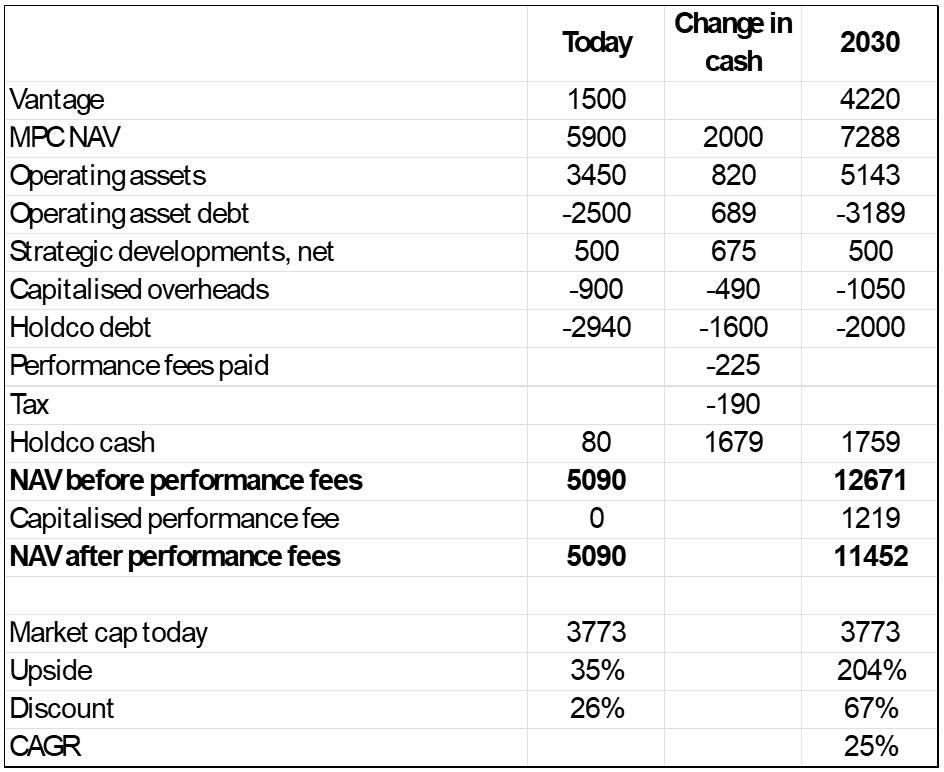

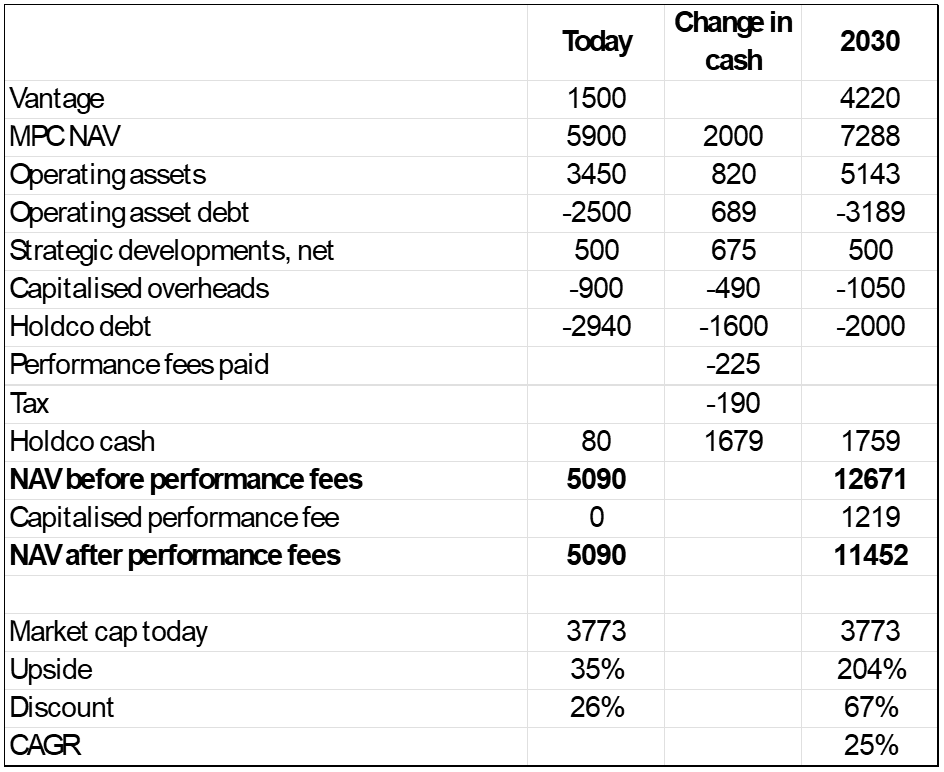

The table below shows my sum of the parts (SOTP) for today, which I think serves as a reasonable bear case, and a bull case for 2030. The column in-between shows cash flow for each segment, which builds up to the 2030 cash balance. Figures are in millions of dollars.

Let’s dive into the detail.

Insurance

In December 2025, Howard Hughes announced the acquisition of an insurer named Vantage, which was founded in 2020 by Carlyle, Hellman & Friedman, and the founding management team.

Insurers make two types of profit (or loss). First, insurers try to charge more in premiums than they pay out in eventual claims. And second, in between collecting the premium and paying the claim, they invest their customers’ money - called float - and keep the returns.

There are two broad strategies in insurance. One is to underwrite programmatically, selling large volumes of less profitable insurance business. This results in high leverage (measured as premiums/equity and assets/equity) and as a result, regulators insist that the assets are invested conservatively. Weak insurance profits and conservative investing produce mediocre returns on assets, but the leverage helps turn this into an adequate return on equity.

The second strategy is to write less insurance, being pickier about the risks taken and the prices offered. This results in higher margins, and also in lower leverage, which has several advantages:

It reduces the impact of investment volatility and adverse reserve developments on regulatory solvency.

It gives flexibility to increase the volume of premiums written during periods of strong insurance pricing.

It improves customer perception of counterparty risk. Customers want an insurer whose cheque always clears.

It allows for optimised asset allocation.

It is this last point that can turn this type of insurer into a compounding machine. This second strategy was pioneered by a company you may have heard of: Berkshire Hathaway. The strategy lowers risks in two ways: it writes far less premium volume per dollar of equity than most insurers, and as a result has lower assets/equity; and it invests its float (i.e. its loss reserves) in cash and short-term Treasurys with little to no duration or credit risk. Because it takes so little risk, regulators allow it to invest its shareholder equity into a portfolio of common stocks. The combined returns from insurance margin, plus interest on float, plus returns on well-selected common stocks, achieved with low leverage and risk, have been the stuff of investing legend - and that is what HHH and Pershing want to replicate with Vantage.

Prior attempts to “replicate Berkshire” by hedge fund managers have not worked. Pershing argue that these were structured principally as financing vehicles, designed to boost funds under management for the fund managers. By contrast, Pershing will charge HHH a fee on its market cap, but they will not charge Vantage a fee for managing its investment portfolio. Their incentive is therefore to create value, not to write additional premiums to increase float and therefore fees for the investment manager, regardless of the insurance returns. Indeed, HHH have been explicit that Vantage will not have any top-down goals for premium volumes: premiums will only be written when the business is judged to be profitable. I think there is a second difference, too. Hedge funds run long/short books, where the longs are typically high turnover and the shorts have uncapped downside that can destroy a fund if they are wrong. There is no fundamental reason why hedge funds should compound - it is all down to the skill/luck of the manager. But Pershing is no longer really a hedge fund. They invest long-only and long term in some of the largest, fastest-growing, deepest-moat companies on earth. While Pershing have an exceptional record of outperforming broader markets, a lot of the compounding simply comes from the holdings themselves.

Because Vantage plans to run with low leverage, float invested in Treasurys, and equity invested in common stock, we can split the valuation into two parts:

The insurance part, which includes selling insurance, paying claims, and interest on float.

The investment part, which is the common stock portfolio.

This is not how most analysts would do it. Most would include the interest on float in the investment bucket, and would then calculate an ROE for the whole company. However, the interest on float is directly related to the amount of insurance written. It is a core part of insurance profits, whereas the returns from investing equity into common stocks is not. The advantage of doing it my way is that we can value the common stock portfolio at market prices and then value the insurance operation standalone.

Why market prices for the common stock portfolio? Because it is easily replicable. Pershing Square have said that Vantage’s common stock portfolio will be transparent and invested similarly to their existing portfolios, in liquid stocks of large companies. This means the portfolio is easy to replicate, and should not be valued higher than market prices even if the returns are spectacular. Pershing disagree with this logic, arguing that it is impossible to replicate the exact timing of their trades, the exact weights in their portfolio, or their occasional highly asymmetric hedges. This is true, but it is clear from the valuation of Pershing Square Holdings, which trades at a persistent discount to NAV, that the market does not see things this way. (Equally, the Vantage portfolio does not deserve to trade at a discount - the PSH discount is justified by fees, which Vantage does not pay.)

Valuing the standalone insurance operation is trickier. Vantage is currently making a 97% combined ratio. This is what most industries would call a 3% EBIT margin: it means that for every $100 Vantage collects in premiums, it pays out 97% in claims and operating costs. Believe it or not, this is actually pretty good: insurance is a commoditised industry and margins are thin.

HHH say that Vantage’s combined ratio will improve over time. They argue that while its loss ratio is good, its expense ratio is not. This is because it is a young business that has not yet achieved scale, so it is not yet fully leveraging its roughly $350m in fixed operating costs. As it grows, its combined (loss + expense) ratio should improve further.

Unfortunately, HHH have acquired Vantage at the end of a long insurance upcycle. Because insurance is commoditised, it is also cyclical. When profits are available, capital enters the market, pushing prices down. When losses are made, capital exits the market, pushing prices up. The key drivers of these cycles are catastrophe losses and interest rates. When (for example) a hurricane wipes out capital in the insurance industry, prices (at least in relevant lines of insurance) are likely to rise. And when interest rates rise (or fall), capital seeking the best risk-adjusted returns leaves (or enters) insurance.

The increase in interest rates after covid, combined with various catastrophe losses, drove a hard market (upcycle) in insurance pricing from roughly 2021-2025. That hard market is now softening. This makes it harder for insurers to write profitable insurance, and is likely to pressure both premium growth and combined ratios across the industry.

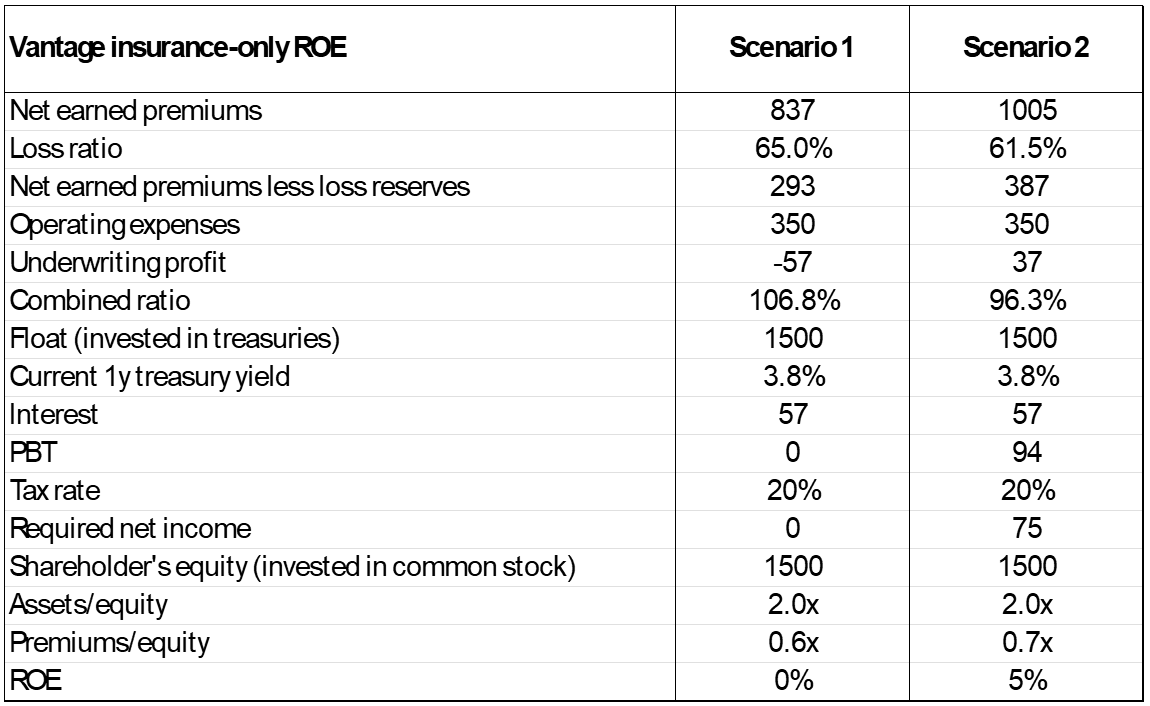

The following table shows two possible valuation scenarios for Vantage. Both assume $1.5bn in shareholder equity, 2x assets/equity, and $350m in operating expenses, which is roughly right for 2q26 according to the deal deck and commentary. The scenarios are:

Vantage writes fewer premiums at a higher loss ratio and achieves zero insurance profit.

Vantage writes more premiums at a lower loss ratio and achieves insurance net profit equal to 5% of shareholder’s equity.

This allows us to frame Vantage’s valuation quite simply.

If Vantage’s shareholder’s equity is invested in common stocks, and we are valuing this portfolio at market price, then we are going to pay 1x shareholder’s equity for the common stock portfolio.

In addition, we are going to pay 10x insurance earnings. 10x is a 10% earnings yield, and if you add inflation you get a low-teens total nominal return. That seems fair for a commoditised business.

For now, while I wait to see how the cycle unfolds and whether Vantage is a good underwriter, I will use Scenario 1 and assume insurance profits are $0. My SOTP today therefore only values Vantage at 1x equity for its common stock portfolio. However if Vantage proves its worth then the insurance operation could easily produce a return on equity of 5%. At 10x, that justifies another 0.5x equity for a total multiple of 1.5x, which is what I use for my 2030 SOTP.

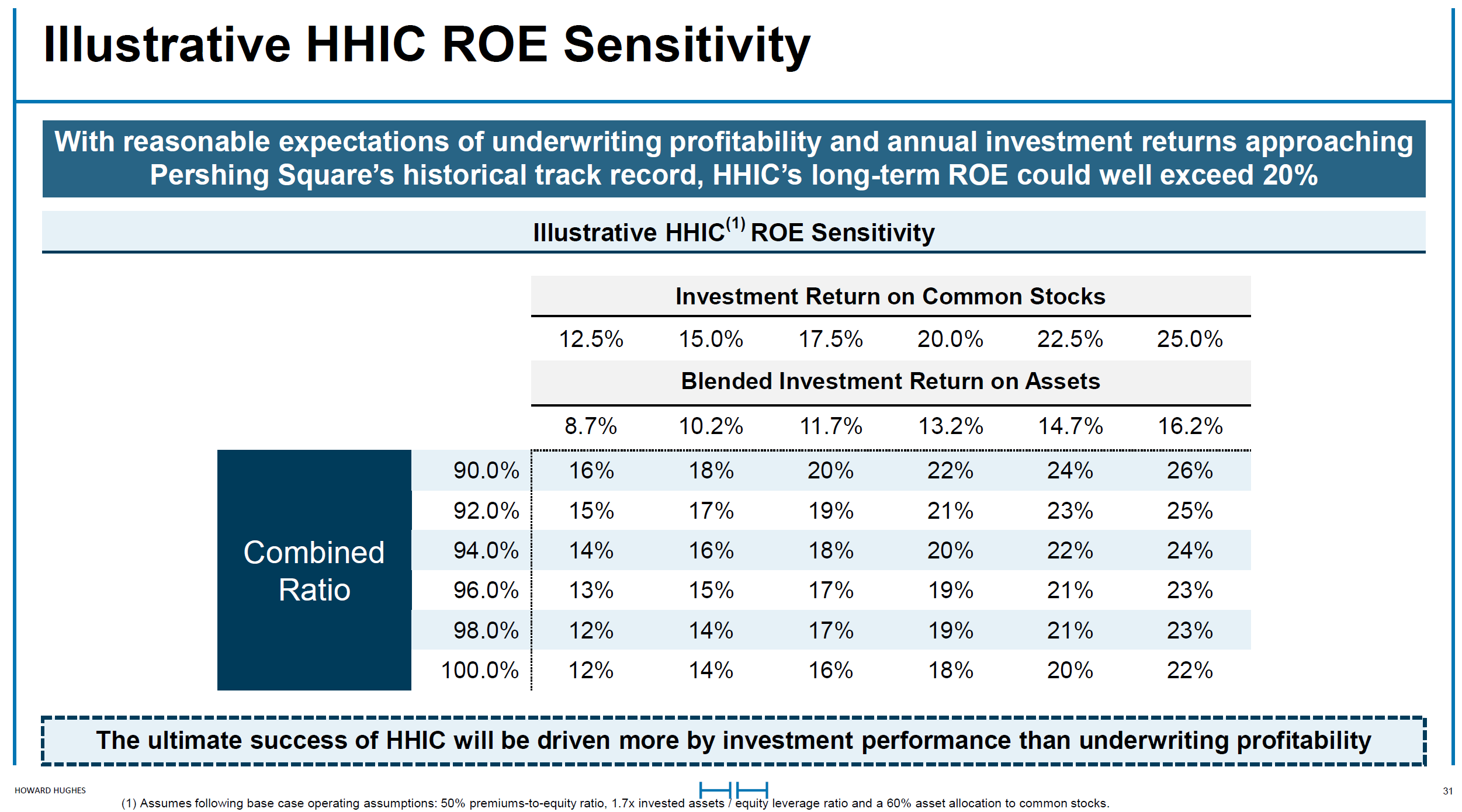

The magic of this model is that it might well produce 20% or 25% compounded returns. Pershing Square say they aim for 20% returns on their common stock investments, and insurance could easily add 5%. This is why excellent insurer-investors like Berkshire Hathaway and Fairfax Financial have produced such exceptional compounded track records over time. Before acquiring Vantage, HHH produced this useful table showing how common stock returns and combined ratios drive compounding (the underlying assumptions about leverage and asset allocation are broadly similar to mine):

Four final thoughts on insurance:

Remember: the common stock portfolio is replicable, so even if it does produce a 20% return, it should not be valued at more than 1x. That’s why I structure the valuation as 1x common stocks + 10x insurance ROE, rather than 10x total ROE.

This valuation includes nothing for AdVantage, which deploys 3rd party capital into insurance policies underwritten by Vantage. This effectively allows Vantage to monetise its underwriting skills via a fee-stream, rather than just by writing policies backed by its own capital. This is very valuable in upcycles but less so in downcycles, and I don’t want to ascribe value to it until we have seen how it performs through cycles.

The big risk not captured in my valuation is if Vantage have dramatically underestimated future claims. In this case shareholder’s equity will be overestimated, since it will be used to pay claims. What gives me some comfort here is that virtually all of Vantage’s book has been written during a hard market which offered good pricing. I can’t guarantee it, but there really shouldn’t be systemic problems in the insurance book.

HHH have said that post-close, they will invest more primary equity into Vantage to de-lever the balance sheet and reduce the effective purchase price (since primary capital will go in at 1x p/bv). I don’t model this because I don’t know the amount, but it doesn’t really change my valuation - the cash merely moves from one of HHH’s pockets to another.

Master Planned Communities

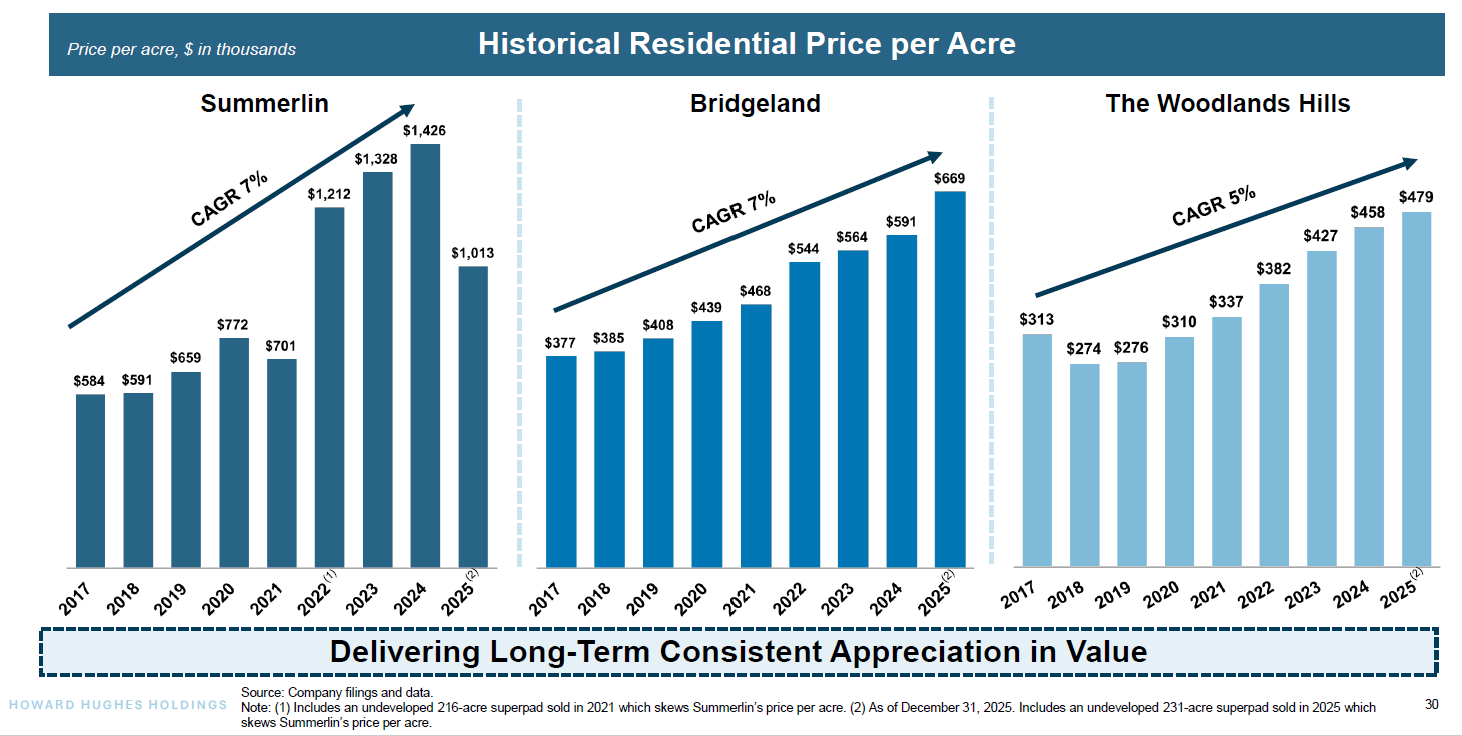

These are large plots of land that are steadily sold to build new suburbs. Howard Hughes adds value by securing permits for long term development plans, building basic infrastructure, building commercial real estate, and controlling supply to maximise profits over time. As these communities mature, the price of land for homes rises dramatically. Development can take decades, with negative cash flow initially and very strong cash flow at the end, when the infrastructure is complete and land values are high.

I like this business. It makes intuitive sense to me that by investing early in a place people are likely to want to move to, investing to improve the area, curating a lovely place to live and work, and monopolising the supply of land with a long term value-maximisation mindset, it is possible to make good returns. Howard Hughes’ MPCs are in affordable areas with low taxes and excellent demographics, and land values are rising steadily:

75% of current MPC profits come from Summerlin (22,500 total gross acres along the western rim of the Las Vegas Valley) which opened in 1990, and another 22% from Bridgeland (11,500 total gross acres in Houston) which opened in 2010. The other MPCs are The Woodlands and Woodlands Hills (Houston) which are smaller but are scheduled to ramp profits over the next few years, and Teravalis (33,800 total gross acres in Greater Phoenix, Arizona), which only started in 2024 and is targeted for completion in 2086. In maturity terms Teravalis is the baby of the portfolio, but it is a very big baby.

HHH give us 3 ways to think about valuing the MPC business. The first two are earnings before tax (EBT), which is a P&L measure, and MPC Net Contribution, which is a cashflow measure. To get from EBT to Net Contribution, the big adjustments are that

Cost of sales is added back. This is what HHH paid to buy the land, so it is a noncash charge in the current period.

Proceeds from MUD and SID bond collections and sales are added back. These are bonds issued by municipalities to HHH to subsidise some of the development expenditures.

MPC development expenditures are deducted - this is the investment to make the land saleable (some of which earns MUD and SID bonds which can be collected or sold in future periods).

The following table shows EBT and Net Contribution. Net Contribution has lagged EBT by an average of $75m per year over the last 4 years due to MPC development expenditures. Eventually, Net Contribution will exceed EBT as communities mature and less development spend is needed. We are not there yet, but it is clear that profits and cash flows are growing and guidance is for that to continue, although 2025 was a bumper year on the sale of a particularly large plot in Summerlin so there is a step down in 2026:

I assume that MPC Net Contribution averages $400m per year over the next 5 years. For the purposes of my 2030 valuation, this means $2bn gets deducted from the MPC valuation and added to the holdco cash balance.

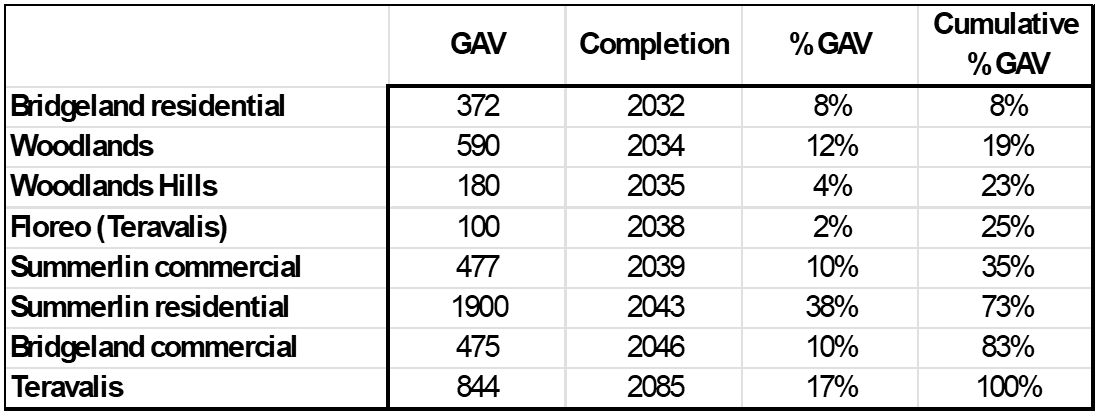

The third valuation measure is Gross Asset Value (GAV), which is a discounted cash flow. The table below shows % of GAV and planned sell out dates for each of the MPCs. By 2036, all of Bridgeland residential and The Woodlands, and Woodlands Hills will have been sold, along with perhaps half of Summerlin. That accounts for around 50% of today’s GAV. By 2046, Bridgeland commercial, Summerlin, and some Teravalis will have been sold, accounting for another ~35% of today’s GAV. By MPC standards, these timeframes are short: we are well into the monetisation phase. This data is from September 2024, which is the last breakdown of GAV that I can find:

The most recent GAV is $4.4bn, from 4q25. This excludes Teravalis because it is from a slide showing GAV growth excluding the acquisition of Teravalis in 2021. Teravalis (including Floreo) had a GAV of $944m 18 months ago. Given the high discount rates on these assets, their GAV is likely $1.2bn today, making a total YE25 GAV of $5.6bn. The segment also has a little over $400m in net cash, but this includes $400m of MUDs. HHH has a habit of selling MUDs at discounts of 20-25%, so I reduce segment net cash by $100m. MPC NAV is therefore $5.6bn + $0.3bn = $5.9bn today.

Should we trust a company-provided GAV? As you might expect, the key inputs to the DCF are aggressive, but defensible:

Commercial land price growth rate 3.5%, fractionally above probable inflation as population density rises.

Residential land price growth rate between 5% and 7% depending on the asset. This is in-line with historical data.

Discount rates of 7-9% for the more mature assets, 15% for Floreo, and 20% for Teravalis. The weighted average in 2024 was 9.6% and this will rise slowly as Floreo and Teravalis grow in the mix.

Cash margins between 75% and 97% - selling land you already own is a very cash generative business!

If I was going to question one assumption, it is the 7% residential price growth rate at Summerlin. This asset accounts for a large part of the overall GAV, and while 7% is in-line with historic performance, extrapolating it for the 17 years until sales are complete is not cautious. Offsetting this is the fact that Teravalis, a monster asset, is discounted at 20%; if it works out it will drive huge GAV upside. In fact, GAV is likely to rise despite accelerating land sales. At 20%, the Teravalis GAV will be $7.4bn in 10 years if everything goes to plan. That exceeds the GAV of all the MPCs today.

Overall I think the GAV HHH provide represents a full, but not crazy, valuation for the MPC segment.

Strategic Developments

This segment develops high-rise condos for sale. The majority of what it is building is at Ward Village in Hawaii, but it is also building the Ritz Carlton Residences, an ultra-luxury condo development in The Woodlands, which might become a template for further developments in the MPCs.

Earnings from Strategic Developments are lumpy. It takes 3-4 years to sell a tower, and the profit is booked at the end; on top of that, a couple of the Ward Village towers are affordable homes sold at cost. That’s why HHH booked $282m of segment EBT in 2024, when it had a high-value tower to sell, and -$14m in 2025, when it had an affordable tower to sell.

Nevertheless, the economics of Strategic Developments are attractive. Most of the towers are pre-sold, which reduces risk. Between deposits and construction loans, HHH has to put up very little equity to get a tower built. They have a decent record of delivering towers on-budget. And they already own the land, so the cash margins are decent. HHH guide to a 25-30% gross profit on sales. After net interest, I estimate 15% pretax margins and 12% net. That’s in Hawaii, where construction costs are high, because labour is tight and materials have to be shipped.

HHH has already delivered 8 towers at Ward Village, 2 of them affordable. It has 2 more under construction and 3 in pre-development. These last 5 are 71% sold on average with $3.5bn in revenue already under contract, which implies $4.9bn in total eventual revenues. In practice revenues will probably be slightly higher, since the final units usually go for the highest price.

The Ritz Carlton Residences are 76% pre-sold with $37m in deposits taken and $380m of revenue under contract, implying total sales of $500m. Working through build cost and likely interest profile I think net margins are likely to be slightly higher here - I assume 15%.

All of these developments will be complete by 2030. $5bn in revenues at 12% and $500m at 15% implies $675m in net profit over 5 years. I discount this to $500m for today’s valuation.

For the 2030 valuation, two things are relevant. First, in early 2025, entitlement changes at Ward Village made another 2.5-3.5 million square feet of development possible after 2030. That’s at least equivalent to the 5 towers currently in development and pre-development. Second, the success of the Ritz Carlton Residences, which generated $250m in future sales in their first week of marketing, is something that HHH might be able to replicate as they build out their MPCs. I therefore assume Strategic Developments, having generated $675m of cash flow between 2026 and 2030, is still worth $500m at the end of 2030.

Operating Assets

This segment owns commercial real estate that Howard Hughes has built in its MPCs. These assets generate rent, but they also make the communities better, which drives residential land price inflation - so while this segment should be valued on its rental profits alone, a significant part of the return on investment from building these assets turns up in MPC segment profits.

The key metric for this segment is net operating income (NOI). This is rental income less cash operating expenses - effectively ebitda for real estate. It’s worth noting that once interest and depreciation are deducted the segment produces slightly negative EBT. One way to think about this is that the value is effectively in the depreciation (which generates cash flow and shields the business from tax) and the underlying land, with an option on the true asset life being longer than that assumed for depreciation purposes.

Roughly half of the NOI is from office, and the other half is a mix of retail, commercial, and multi-family. There is obviously debate about what assets like this are worth, especially office. My view is these are advantaged assets because they are located in thriving, growing residential communities and because Howard Hughes controls nearly all the commercial real estate in their MPCs. They rarely sell, and nobody else can build without their permission, so there is little risk of speculative overbuild. The downside is that HHH cannot sell a controlling stake, at least not until the MPCs are complete, although they have speculated that they could sell a minority stake in Operating Assets which would set a valuation marker and produce cash for reinvestment.

HHH reported $276m of operating asset NOI in 2025, and the company says stabilised NOI for existing assets and those under development will be $361m, with the vast majority of the uplift coming from existing assets that are not yet mature. The company does not say when stabilised NOI will be achieved, but the asset-by-asset disclosures suggest that it should take 3-5 years. For today’s valuation I assume the $262m in 2025 NOI is capitalised at 8%, and for the 2030 valuation I capitalise the $361m in stabilised NOI at 7%, on the basis that more mature assets in more mature communities should be worth more.

Notably, neither valuation assumes any franchise value in Operating Assets - yet it is highly likely HHH will continue to create value by building new assets.

Roughly, segment NOI less depreciation and interest is zero. With no EBT, there should be no income tax to pay. I therefore assume segment free cash flow (FCF) is equal to depreciation - roughly $170m per year - and add 5x$170m in cash flow from Operating Assets to the 2030 cash balance, less $30m for additional equity needed to complete assets under construction. I do not grow FCF with NOI, which should be conservative. In addition, I model 2030 segment net debt at 62% LTV (the company guides to 60-65%). The increase in debt from $2.5bn today generates an additional $689m of cash for HHH.

Holdco debt

HHH break out debt by segment in the 10k. There is $2.04bn of debt at the holdco level. The Vantage deal will cost $2.1bn, and HHH had $1.28bn of cash at the holdco level at YE25. I assume $1.2bn of this is spent, and therefore $0.9bn of Vantage prefs will be issued to PSH, for a total of $2.94bn in holdco debt and prefs by mid-2026.

Some notes:

HHH claim the MPCs are unencumbered; I think this is wrong: both the Operating Assets and Strategic Developments carry as much debt as they can bear. The MPC segment has very little, but the holdco has quite a lot. In effect, the MPC debt is simply at the holdco level.

The debt is well-structured: in terms of interest rates, 96% is fixed or swapped or capped, and after a $1bn bond issue in February 2026, ~60% is due after 2030.

HHH has the option to buy back the Vantage pref at a price linked to the growth in Vantage shareholder’s equity. I assume these prefs are repaid in 3 equal annual instalments (consistent with guidance) and grow the balance by 15% per year because I assume Vantage shareholders’ equity grows at this rate for my 2030 valuation.

Overheads

HHH guide to $82-92m in overheads in 2026. I assume $90m and capitalise this at 10x. I also assume overheads inflate at 3% per year, which feeds into my cash projection and my capitalised overheads figure for 2030.

Overheads includes the fixed component of the Pershing Square fee, which is $15m per year inflated by the Personal Consumption (PCE) index.

A couple of key items are not included in overheads:

Deal fees, which could be significant if HHH pursues a lot of deals.

Stock based comp. I prefer to think about this in terms of potential dilution rather than the Black Scholes based P&L measure. There are 59m shares outstanding. No options were issued in 2025 and at year end there were 68k options outstanding, so options don’t represent a big dilution risk. 300k RSU’s were issued in 2025 at an exercise price of $77. Assuming RSU issuance continues at this pace and all are exercised, shareholders will suffer 0.5% dilution per year. I can live with that, especially considering Pershing has an incentive to keep stock based comp within sensible bounds (see below).

Performance fees - and Pershing Square’s alignment with minority shareholders

Overheads does not include the variable part of the Pershing fee, which is dependent on the share price. Specifically, Pershing gets 1.5% of the market cap over a threshold. The threshold is calculated by multiplying a fixed share count of 59.4m by a reference share price of $66.15, which inflates with the PCE index. In effect, Pershing can only increase its fee by increasing the share price above inflation. And notably, Pershing:

cannot increase its fee by causing HHH to issue more shares.

can increase its fee by causing HHH to buy back shares below intrinsic value, if doing so increases the share price.

I think HHH directors did an extremely poor job of negotiating the reference price. HHH has argued for years that their real estate business is worth over $100, but now HHH will pay a fee for any share price increases above $66. If the market merely comes to agree with HHH about the value of the real estate business, Pershing will collect a performance fee. That is not right. The reference share price should have been at least the $100 that Pershing themselves paid to inject new capital into HHH in 2025, and ideally $118, which was the NAV that HHH published in 2024 - and even this would have ignored NAV accretion in 2025.

However annoying this is, the fact is that the reference price is $66, and we must assess value on that basis. For me, the key is that there is strong alignment between Pershing and minority investors:

the variable fee clearly incentivises Pershing to increase the share price significantly and sustainably ahead of inflation.

the fixing of the reference share count incentivises Pershing to make (or influence the HHH board to make) shareholder-oriented decisions around share issuance, buybacks, and stock-based comp.

PSH and PSCM between them own 47% of HHH. Ackman and his team own 90% of PSCM and 27% of PSH. Indirectly, they own a lot of HHH. They want the share price to compound.

HHH is reputationally deeply significant for Ackman. He has often spoken of his admiration for Buffett and desire to build one of the great investment track records. To compound an insurance holding company for decades is to be compared to the Master. I doubt much motivates him more (except fees).

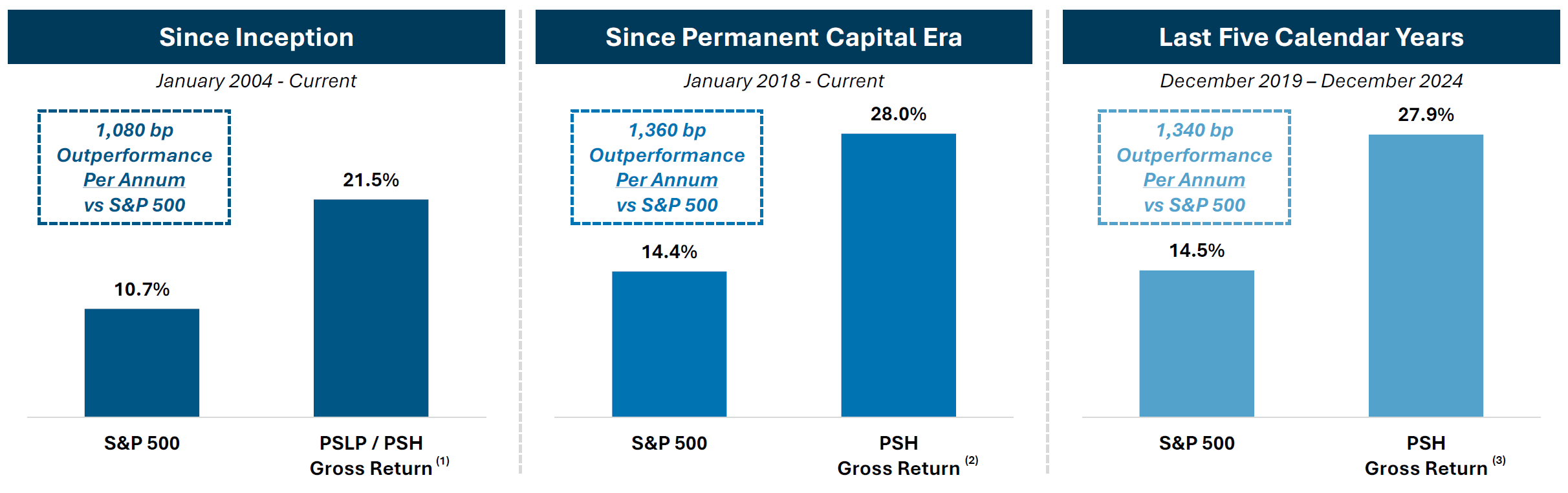

Pershing Square have several advantages over other fund managers. In particular, their assets under management is almost entirely permanent. Having managed both permanent and temporary capital, I can attest to the sad fact that capital duration affects manager psychology. It is much easier to focus on the long term when you have permanent capital. In addition, Pershing’s ability to attract talent is significant and their analyst tenure is impressive, which speaks to the culture at the firm. Finally, their performance is phenomenal - the chart below shows gross performance, which is relevant to Vantage, since it does not pay fees:

In short, while I think the HHH directors have done minorities a disservice with the reference price, I think Pershing Square is an excellent and aligned partner.

For the variable fee, my SOTP assumes:

$0 today, since the share price is below the reference price.

A $120 share price on average over the next 5 years, driving a total cash outflow of $225m.

That in 2030, the share price equals the NAV, maximising the variable fee, and that the fee is capitalised at 10x.

Tax

Within my NAV, insurance, MPCs, and strategic developments are valued net of tax, and the operating assets make no earnings before tax so they pay no tax. I therefore do not capitalise future tax into the NAVs.

I do, however, deduct tax from the cash flows as follows: $400m in MPC EBT, less approximately $225m in holdco costs and interest, gives $175m in taxable profits each year, at a 22% rate.

Holdco cash

YE25 holdco cash was $1.28bn and I assume $1.2bn is used for the Vantage acquisition, so my starting holdco cash balance is $80m.

I exclude restricted cash. This is mostly condo deposits so including it risks double counting cash flow from Strategic Developments.

I then add the cash flows from each of the segments over the next 5 years to get to the 2030 cash balance. The striking possibility is that even after buying Vantage, HHH might have $1.7bn to deploy into new acquisitions over the next 5 years, before considering leverage.

Conclusion

First, a confession. HHH is a complex beast, with 4 quite different businesses and an unusual partnership and fee stream to consider. In addition, while the company produces a lot of disclosure, it isn’t presented as clearly or as consistently as I would like. To research HHH is to make multiple choices about what matters, and what does not; what merits more time, and what does not. I may well have missed things, and I apologise if I did.

As I write HHH trades at $63 per share. Recall that HHH thought their NAV was $118 per share in 2024 and Pershing paid $100 per share in 2025. According to my maths:

The stock has 36% upside to my current SOTP.

The stock has ~200% upside of 204% to my 2030 SOTP, a CAGR of 25%.

Here’s a reminder of my SOTP:

And here is a summary of the assumptions:

I don’t expect the stock to rise 36% to its current NAV any time soon. It has traded at a discount for years. But I do think the 2030 NAV is realistic. Not conservative, perhaps, but realistic. I assume good performance from each of the assets, but not spectacular. Vantage shareholders’ equity could easily compound faster than 15%. MPC NAV might not beat my assumption, but with 50% of today’s GAV being sold in the next 10 years the duration of the cash flows will shorten considerably, reducing risk and helping the stock trade closer to intrinsic value. I assume operating assets reach their guided stabilised NOI, but not that any more assets are built. I assume future strategic developments achieve similar economics to current ones, not better, and that the Ritz Carlton Residences success can’t be replicated elsewhere in the MPCs. And I assume $1.7bn of accumulated cash sits on the balance sheet, undeployed.

My standard hurdle for investments is 15%, which compounded is a double in 5 years. Here we can buy a solid set of assets, trading at a discount to a relatively conservative current NAV, with realistic line of sight on making 3x our money over 5 years and compounding after that, because MPC GAV will continue to grow and because HHH now has a virtually infinite reinvestment runway.

Could things go wrong? Could the Vantage balance sheet be littered with huge unforeseen claims? Could the MPCs suddenly lose momentum, perhaps because of large unforeseen demographic shifts? Yes. Of course. But investing is about embracing uncertainty, deciding what risks you want to take, and ensuring you are being paid to take them. On that basis, I am happy owning HHH at $63 per share.

Links to previous work

Thanks for reading - if you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete

This is one of the more rigorous investment write-ups I've come across on Substack. The sum-of-the-parts approach is the right framework for a conglomerate this complex, and Pete's transparency about assumptions at every layer — discount rates, growth rates, combined ratios, capitalization multiples — gives you enough to disagree with specific inputs without dismissing the whole thesis. The Berkshire replication question is the heart of this. Every generation of investors produces someone who wants to build the next Berkshire, and virtually every attempt has failed. Pete identifies the right reasons why — most prior attempts were financing vehicles for hedge fund fee extraction, not genuine long-term compounding structures. The Pershing fee arrangement is better aligned than most, but the reference price issue is a real concession that minority shareholders are subsidizing. Acknowledging that while still building a constructive case is the kind of honest analysis that's rare in public stock write-ups. The MPC business is the part I find most compelling and most underappreciated. A 50-60 year buildout timeline with monopolistic control over land supply in growing metros is a genuine structural moat. The Summerlin 7% residential price growth assumption over 17 years is the input I'd scrutinize hardest — that's a long extrapolation in a single metro, and Las Vegas has historically been more cyclical than most Sun Belt markets. The real test is whether Ackman can resist the temptation to get clever. Buffett's compounding came from decades of disciplined, often boring capital allocation. The Pershing track record is exceptional but built on a concentrated, high-conviction style that's produced spectacular volatility alongside the returns. Berkshire's durability came from boring consistency. Whether Pershing can deliver that over decades is the open question no spreadsheet can answer. For anyone following HHH — what's the one assumption in the thesis that would change your mind if it broke?

Thanks for a great article