Review: Uber in 20 years

The good, the bad, and the skew.

Summary

What it does: Orchestrates mobility.

Elevator pitch: Uber is a dominant 3-sided network that allows customers to order transport and hamburgers.

Mental model: Scaler, moat, asymmetric payoff.

Valuation and potential returns: 30x non-GAAP net income, but potential to compound in the teens for 20 years.

Exchange and ticker: NYSE, UBER

Stock price and market cap: $78, $154bn.

Do I own it? Yes.

IR website: here.

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

Tl;dr

This is a thought piece about Uber’s TAM and competitive position in 10 and 20 years. The underlying product should become far cheaper and therefore the market far larger. Autonomous vehicle (AV) supply is likely to fragment, meaning many providers will need Uber to scale and compete. AI personal assistants might come to dominate demand, creating a risk of disintermediation, but there are strong practical and regulatory reasons why assistants will not bypass Uber. Uber should probably engineer its take rate down to help grow the market and reduce the risk of disintermediation, but even so there should be plenty of space for revenue growth and operating leverage. The resulting skew between more bearish and more bullish investor outcomes is attractive.

Introduction

Investing requires a balance between attention to detail now and a broader, more general understanding of how the long term future might unfold. This piece attempts to imagine how Uber’s competitive moat might evolve over 10-20 years in the face of two interrelated threats: the growth of AV platforms, and disintermediation by AI.

For a more traditional introduction to Uber, packed with details on current market shares and financials, I recommend this by HatedMoats:

For long term investors in Uber, I think there are 5 things that really matter:

Potentially explosive growth in the total addressable market (TAM).

Whether the autonomous vehicle systems market fragments or is winner-take-all.

Whether AI can disintermediate Uber.

What happens with take rates.

The upside/downside skew.

Let’s ride.

TAM explosion

AVs will massively expand Uber’s TAM, because they will massively reduce the cost of transport.

Why?

AV drivers will be much cheaper than human drivers. This reduces the cost per mile.

AV technology enables a wholesale shift from personal use toward rideshare. This will dramatically increase utilisation of the global car fleet: personal cars get used about 5% of the time, whereas cars on Uber achieve 3-4x that, and without driver fatigue AVs will achieve more. Since depreciation is a significant part of total cost and is fixed, higher utilisation of the global fleet further reduces cost per mile.

AVs can be owned in fleets. Part of the cost of individually-owned cars is personalising them. Colour, trim, and specification choices all add complexity and cost. Fleet-owned cars can be mass-produced to exactly the same design, further reducing cost per mile.

AVs will be safer than cars driven by humans and as discussed, the cars will cost less. This brings down the cost of insurance. In addition, AVs will eventually bring down the cost of regulatory compliance, broadly defined. No more sexual assaults or risk of drivers being classified as employees. All these things further reduce cost per mile.

Electric vehicles are more expensive to buy than infernal combustion vehicles, but less expensive to run and maintain because they have 1/10th the number of moving parts. As utilisation rises the fleet will naturally shift towards EVs, further reducing cost per mile.

Large numbers of autonomous electric vehicles (AEV) solve one of the world’s great problems today: renewable electricity is cheap on a levelised cost basis but intermittent, and when you include the cost of storage or backup it’s expensive. EVs are batteries on wheels. An AEV can constantly compute the highest-value use between charging, discharging, and mobility. This will require significant investments in local grids, but the societal benefit is compelling. AEVs will get paid for balancing grids, further reducing cost per mile.

AEVs will have AI inference chips on board. These chips will be idle when the car is not driving. This idle time will represent a large distributed compute capacity. It won’t be the most efficient compute, but the marginal cost will be tiny, so it’ll get used. AEVs will get paid for distributed compute, further reducing cost per mile.

Uber’s user base is relatively small today. Its annual active user count is roughly half Spotify’s monthly active user count, despite the fact that Spotify arguably has more competition (Apple, YouTube, and Amazon are all huge in music streaming). Why? Because Spotify is free. Uber’s user base is fundamentally limited by the high marginal cost not of its service, but of the product it distributes. Most people can’t afford to use taxis and food delivery very often, and many not at all. The scope for TAM growth is absolutely massive: taxis and ridehailing likely account for less than <1% of distance travelled by humans on land, whereas personal cars likely account for >70%. As cost per mile comes down, I would expect total distance travelled to rise and ridehailing to gain share. For many people, I expect ridehailing to replace car ownership entirely, eventually. The potential for TAM expansion is enormous: if I am right the user base will explode and frequency will rise.

The above focuses on mobility, but the same applies in delivery. The human driver represents about half the cost of last-mile delivery. Robotics will transform this. Uber has partnerships with Nuro, Lucid, and Serve to introduce AVs and robots for delivery. The impact on total cost will not be as significant as it might be for mobility, because the underlying cost of the hamburger being delivered won’t change, but reducing the cost of delivery itself will expand the market.

These changes have a number of broad societal benefits, too. Driving becomes safer. Cities become more liveable: without personally-owned cars, inner-city parking can be eliminated and roads can be re-designed with larger walkways and cycleways. Carbon intensity is reduced. I think it is likely that, in time, AV will receive both regulatory and popular support.

Pushbacks:

“I want to keep my car. I like driving”. Do you, though? Really? I get that taking a Ferrari round Silverstone or going off-roading in a Land Rover is fun. But driving to work? Driving with your kids screaming in the back? These things are not fun. Given the choice most people would far rather sit in the back, do some work, make a call, watch a film, play with the kids, or just stare out of the window.

Specific use cases. You might use fleet AEVs on Uber for your commute, but not for heading out of town at the weekends, and definitely not for your annual half term ski holiday drive from London to the Alps. But I think that as cost per mile falls, as fleet AEVs become ubiquitous, and as Uber innovates around specific use cases and availability in less-dense areas, you’ll book AEVs to do exactly those things. That half term ski trip? You’ll book 2 AEVs 6 months in advance for the whole week, and it’ll still be cheaper than owning a car.

I am not arguing any of this will happen soon. This is a multi-decade, high-level prediction. But I think the logic is compelling, and that the change will accelerate as the cost benefits become clearer.

AVs - fragmentation vs dominance

Uber will benefit from TAM expansion if it is the demand aggregator for multiple AV types and fleets. It will not benefit if two or three AV manufacturers dominate the market and build their own demand platforms.

In this, I feel pretty confident. I think fragmentation is likely for a variety of reasons:

The market is huge. Huge markets attract competition.

None of the up-and-coming AV manufacturers has a pre-existing advantage: a product that is miles ahead, ownership of all the data or all the customers, or vast amounts of sunk capital that others have to match to catch up.

There’s no real barrier to entry in car manufacturing, a famously commoditised industry.

There’s no real barrier to entry in support infrastructure (charging, etc.).

There’s no real barrier to entry in developing AV systems. This is more controversial, but it is already clear that multiple players are developing AV datasets and/or the ability to train AV models in virtual worlds. Also, the challenge does not lend itself to having one winner: in the long run it’s not about being the best, but about being good enough. I think many AV systems will eventually meet that hurdle.

Several powerful entities are highly motivated to ensure no one AV system dominates, including Uber, NVIDIA, regulators (for competitive reasons), and governments (for security reasons). NVIDIA’s full stack AV offering and Uber’s Autonomous Solutions are great examples of how these two companies, at least, can be agents of fragmentation - not just beneficiaries of it.

Assuming the market does fragment, Uber is a huge beneficiary. Utilisation will be the holy grail of AV economics and it will not be possible for every player to develop a demand platform - they will need an aggregator. Uber is positioning itself as a plug-and-play monetisation platform for AV. It offers instant utilisation, dispatch, operating and finance partnerships, customer support, and localised compliance. As a result it has a rapidly growing array of partnerships with AV developers and legacy car manufacturers, all aimed at launching AV fleets in multiple cities worldwide over the next few years. These solutions may not be the best or cheapest initially, but Uber lets them monetise quickly and reinvest to improve. For details on Uber’s partnerships (and links to some interesting models), I recommend this by Thomas Reiner:

Uber takes a lower percentage of gross bookings for AVs (the target appears to be around 20%) than it does for human drivers (around 30%). However, it also has lower driver incentive and insurance costs. In the article below, Manu Invests estimates that Uber’s “real net revenue” might be as much as 65% higher with an AV driver than it is with a human one. I would add that if sales, marketing, R&D, G&A, and D&A costs remain the same, all of that drops to the EBIT line. Applying this assumption to 2025 financials implies that shifting to AV could nearly double EBIT (assuming only mobility benefits - if the other segments do, too, EBIT could triple).

Uber’s economics also work for AV fleet operators. Uber takes 20% of their revenue. In return, it delivers higher revenue and lower costs than they can generate on their own:

With Uber, fleets don’t need to acquire customers. My guess is that most startups would need to invest >>100% of revenues for years to match the utilisation that Uber can provide on day 1 - something investors simply will not support in a market with so many players and no evidence of winner-take-all characteristics.

Uber estimates it generates 30% higher utilisation than standalone AV operators are achieving, and believes that the gap will grow from here because the standalone operators are currently running small fleets in very high-demand areas, with free publicity and novelty value on their side. These ideal utilisation conditions fade as fleets grow and AV expands into less dense areas.

Nevertheless, some players will go it alone and build their own demand platforms. Successful standalone players will have two key things in common: deep pockets, and cheap customer acquisition costs as a result of existing brand awareness and legacy apps. In the west, Tesla’s Robotaxi and Google’s Waymo are the obvious candidates. For these players, going it alone may be a rational choice: saving 20% of revenue in the long run justifies the investment to acquire customers today. But even in these cases, selling spare capacity on Uber to maximise utilisation will probably make sense. And even advantaged standalone players do face two challenges:

They will grow city by city, and it will take years to match Uber’s coverage. Uber is using that time to become the demand aggregator for dozens of other AV fleets.

Users simply don’t want too many ridehailing apps. My home in London is in a ridehailing blackspot. I often have to search on 3 apps to get a ride, and I absolutely hate it. It is stressful and often expensive, because if I get distracted I can easily end up with two rides and a cancellation fee. I recognise that competition is necessary, but I would far rather consolidate my usage onto one app.

My guess is the vast majority of demand will settle onto a maximum of 3 apps per area. The network effects in this business are primarily local, so not everywhere will have the same winners, but Uber is very well positioned. Certainly if Waymo and Tesla came to London at scale, I’d stop using FreeNow and Gett instantly - but not Uber.

For these reasons, as long as consumers use apps to hail rides, I am pretty confident Uber will be a dominant player. And therein lies the problem. What if consumers don’t use apps?

Can AI disintermediate Uber?

The Dutch Investors recently wrote an excellent article on how hard it was for Uber to build its network, and therefore how hard it would be to disrupt.

As an Uber shareholder, reading this felt like slipping into a warm bath of confirmation bias after a long day. But unfortunately, I can imagine how it might be wrong.

Uber’s network connects millions of drivers with hundreds of millions of consumers. The marketplace is incredibly fragmented. That’s why the network was difficult to build. But even in a fragmented AV world, supply will consolidate down to a few AV fleets. And if AI personal assistants (AIPA’s) get better - which they certainly will - the demand side could consolidate too.

In other words, if the future of ridehailing is AV and “Hey, Siri”, there might only be a few dozen major fleet providers on one side of the network and 3-4 AIPA’s on the other. That makes the network much easier to replicate. If the AIPA’s develop direct links to the fleets, they could bypass Uber entirely. This worries me much more than the AV transition because fewer people seem to be focused on it.

Notably, Uber cannot counter this threat with “hey Uber”. The operating system providers do not allow the creation of always-on wake words at the OS level, partly because they gain a huge advantage by keeping this functionality to themselves, and partly because there are data security implications of always-on listening so they can’t let everyone do it. There is a workaround in Android, but it requires running a foreground service with persistent notifications, isn’t optimal for battery performance, and is rarely used. So in practice “hey Uber” is only usable when the app is already open, which won’t beat “hey Siri” in terms of user experience.

Nonetheless, I think Uber has a number of potential defences.

The first is that the AIPA’s might route demand through Uber rather than bypass it, and indeed they already do - you can access Uber’s services through Siri, Alexa, and Google Assistant today. There are two very good reasons for AIPA’s to do this:

To reach their full potential AIPA’s will need to offer great services across a wide range of activities, not just mobility. The best way to do this is probably not to take everything in house, but to have specialist providers who excel in each area.

If AIPA’s start disintermediating the orchestration layers in major industries, they will become dominant consumer gateways with extraordinary power across large areas of the consumer economy. I highly doubt that competition regulators will allow this.

The second defence is that to disintermediate Uber, AIPA’s would have to orchestrate mobility themselves, dynamically predicting demand, optimising routes, booking rides, negotiating prices, and supporting customers. They would have to do this well enough to offer better economics to fleets than Uber, despite the fact that the fleets would have to take the lead on building support infrastructure partnerships and navigating complex and varied local regulations, things Uber currently helps with. Uber’s vast datasets, deep experience, and emerging partnerships in these areas represent a deep moat. For more on what Uber does under the hood, I recommend this by Hidden Market Gems:

A third defence is that Uber is actually a 3-sided marketplace. While supply and demand for mobility might get consolidated, it’s harder to imagine the same happening to delivery. AIPAs might be able to replicate a significant part of delivery by connecting to major chains, but a large part of delivery will always be fragmented amongst thousands of mom & pop restaurants and shops. Replicating these relationships would be costly.

The fourth defence is time. Consolidation down to a few players on either side of the network is going to take years. Major braking factors are the ramp-up of AV vehicle production, the optimisation of AV designs to bring down costs, the slow creep of regulatory acceptance, and the expansion of AV outside of major city centres. In the meantime, mobility is clearly going to be a hybrid of AV and human, which is much harder for the AIPA’s to replicate.

This combination of defences gives Uber a deep moat, full of crocodiles. Is it unbreachable? Theoretically, no - very few moats are unbreachable in the fact of a deep-pocketed and determined competitor. But it is a huge deterrent. It seems very likely that the easiest thing for AIPA’s will be to route demand through Uber, and that Uber has time to adapt, deepening its relationships with AIPA’s, ensuring it is the default API for mobility, and - perhaps - reconsidering its take rate strategy.

Take rates

As cost per mile falls and TAM expands, there are three possible paths for take rates.

Uber’s take rate could stay the same in absolute dollars. Markets might celebrate this in the short term but it would be a disaster in the long: eventually Uber would represent the majority of the cost of a ride, and network participants will be motivated to bypass Uber.

Uber’s take rate could stay the same in percentage terms. This would be very good for Uber’s profits, since we expect the TAM to expand explosively and many of Uber’s operating costs are somewhat fixed.

Uber’s take rate could come down in percentage terms. This would be less good for profit growth but phenomenal for Uber’s competitive sustainability.

This might not be a popular view, but I will be very bullish if Uber finds intelligent ways to manage its take rate down as gross bookings inflect upwards. Of course, I will not be bullish if this happens chaotically under intense competitive pressure. But win-win solutions, in which (for example) Uber offers lower take rates to fleets that dramatically expand low-cost supply in strategic areas, would be a very good outcome. If it does this, Uber will combine three of my favourite competitive moats:

Network effects, which Uber already has.

Scale economies shared, in which economies of scale are shared with customers in the form of lower prices, which drives more demand and more economies of scale which are also shared, creating a powerful flywheel.

The cheap critical component, in which some critical component is so cheap that nobody even thinks to replace it or compete with it, but it is still priced to give excellent returns to its provider.

Valuation and skew

I think investing is about embracing uncertainty. Many investment writeups predict what will happen. My view - especially at a time of rapid and accelerating technological change - is that we simply don’t know, and we need to be comfortable with that. What we can do, however, is frame different long term futures and assess risk-reward skew.

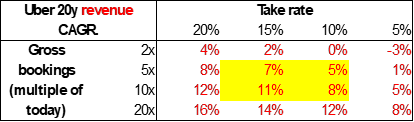

This table shows what would happen to Uber’s 20 year revenue CAGR under very different gross billing and take rate scenarios:

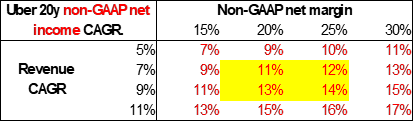

The next table takes the revenue CAGR range in yellow in the table above, and shows the resulting 20-year non-GAAP net income CAGR under different margin assumptions:

Some thoughts on the inputs:

As discussed above, I would like to see take rates trend down over time.

Gross billings grew 19% in 2025 without any real help from falling cost per mile. Over the next 20 years I would expect cost per mile to fall hard in real terms; as a result total distance travelled will grow ridehailing will take a much larger share. I can only guess at the impact, but I think gross billings could easily grow +/-10x under those conditions. I don’t have a strong view on whether mobility outgrows delivery, so I apply the growth to consolidated gross billings.

Net margins. In 2025, Uber reported a 10% non-GAAP net margin. There are 4 reasons to expect this to increase: 1) as discussed above, AV economics may drive up to 2-3x greater EBIT for the same level of gross billings; 2) Uber has significant fixed costs, creating strong operating leverage as revenue grows; 3) AI should enable productivity increases, and 4) freight is currently almost 10% of revenue but lossmaking - this will presumably either scale to profitability or be closed.

This is obviously not a sophisticated analysis - indeed, I imagine it gives the detail monkeys among my readership the yips - but I find it useful for framing skew.

In the lower scenario, with 5% revenue CAGR and 15% margins, net income compounds at 7%. Uber currently trades at 30x non-GAAP net income, so the multiple would almost certainly fall in this scenario, but the deployment of free cash flow into buybacks and dividends would help. Investor outcomes would be poor, but not terrible.

In the middling scenarios, with 5-10x growth in gross bookings, 10-15% take rates, and 20-25% non-GAAP net income margins, net income compounds in the low teens for 20 years. In this scenario, I would expect FCF deployment to more than offset any multiple compression.

In the more optimistic scenarios, 11% revenue growth and 30% net margins generates 17% non-GAAP net income CAGR. With buybacks and dividends the compounded returns could be spectacular.

In short: I like the skew.

None of these scenarios represents the absolute worst or absolute best possible outcomes. In the worst case, Uber might fail completely, in which case investors will lose their money. On the other hand, the top table suggests revenue could grow faster than 11%, driving non-GAAP net income compounding at over 20% before FCF deployment, in which case investors could make 40-80x their money. This is the beauty of equity investing: the downside is capped, but the upside is not. I don’t plan on either of these last two scenarios, but if I had to pick, I’d say the second is more likely than the first.

Again: I like the skew.

Links to previous work

Thanks for reading - if you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete

I think regarding point 6, Uber's own history of consolidating fragmented rideshare into 1 major operator suggests governments do like 1-3 major players because its easier to keep an eye on it. Maybe this implies that the 1-3 major AV networks also is more likely. The regulation is what changes the economics more than the free market in this space.