Thesis update - Uber: is Uber Freight a winner?

Uber Freight: disruptor, or mirage?

I recently read an article suggesting that Uber’s opportunity in freight was greater than its opportunity in mobility and delivery. I’m a pretty big bull on Uber’s opportunity in mobility, so that claim caught my eye and I decided to examine it further.

Uber Freight has two parts:

Digital freight brokerage was launched in 2017 and operates as a marketplace; shippers post loads and carriers accept them through the Uber Freight app. Uber earns the spread between what it charges shippers and what it pays carriers, so it is exposed to spot pricing cycles.

Managed transport is a SAAS+services business which manages the entire carrier network for large shippers. This is deeply embedded into sticky customers and is insulated from spot pricing cycles.

Uber Freight’s right to win

Freight is a large and potentially attractive business, but it’s highly competitive with established scale players.

Uber’s 10k states: “We believe that Freight is revolutionizing the logistics industry. Freight powers a managed transportation and logistics network and connects Shippers and Carriers in a digital marketplace to move shipments while leveraging our proprietary technology, brand awareness, and experience revolutionizing industries. Freight provides an on-demand platform to automate and accelerate logistics transactions end-to-end while providing visibility and control of logistics networks. Freight connects Carriers with Shippers’ shipments available on our platform, and gives Carriers upfront, transparent pricing and the ability to book a shipment with the touch of a button. Freight serves Shippers ranging from small- and medium-sized businesses to global enterprises. By leveraging logistics solutions expertise and value-add solutions, Freight enables Shippers to create and tender shipments, secure capacity on demand with real-time pricing, and track those shipments from pickup to delivery. Freight operations are principally based in North America and Europe. We believe that all of these factors represent significant efficiency improvements over traditional transportation management and freight brokerage providers.”

“Revolutionising.”

“Significant efficiency improvements.”

This sounds good.

Is it reflected in the evidence?

Not really:

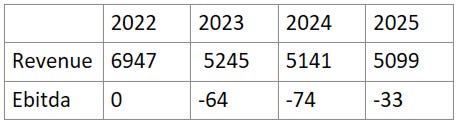

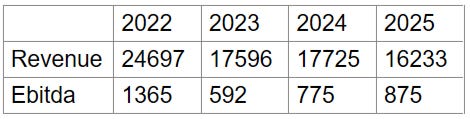

Now in fairness, freight is a cyclical industry. 2023 saw a post-covid boom in shipping rates that boosted revenue (but apparently not ebitda). 2023/4/5 saw a predictable hangover which may be masking progress in revenue growth and margins at Uber Freight. CH Robinson is a competitor in the brokerage industry and shows a similar cyclical trend:

Three things strike me from these figures:

Even allowing for the cycle, Uber Freight shows no obvious evidence of being a disruptive technology that’s “revolutionising” an industry.

Uber Freight appears to be subscale, at least compared to CH Robinson.

CH Robinson is far more profitable than Uber Freight, despite focussing on brokerage, supposedly the lower-quality part of the business.

Going deeper

It is tempting to point to obvious inefficiencies in logistics and conclude that technology - and specifically, Uber’s technology - can solve them. However:

Uber Freight is not uniquely positioned to address inefficiencies in logistics - as I discuss below, there are multiple large players with decades of data and plenty of capital who are building solutions, too.

Some of the inefficiency is structural, creating the illusion of opportunity where in fact there is none. We will never get to the point where every truck is full all the time and no load ever has to wait. It is physically impossible.

Brokers match people who need something moved to people who have a truck. In theory there is a network effect here: the bigger the network, the easier it is for the broker to minimise inefficiencies such as half-empty runs and long journeys to collect loads. However there are no barriers to entry in freight brokerage, and there is no evidence to suggest that network effects are strong enough to drive winner-take-most dynamics. There are an estimated 16,000 brokers in the US. The top 10 firms control about a third of the market. Beyond that, brokerage is wildly fragmented. Even tiny players can build local networks strong enough to keep them alive. In addition there are “load boards”, neutral marketplaces where loads can be posted and accepted, which allow small brokers to widen their reach and also allow shippers and truckers to find each other without brokers at all.

The big brokers (CH Robinson, RXO, J.B.Hunt, etc.) are large, well-capitalised, and very capable of keeping up in the technology race. The same goes for the dominant load board (DAT One, owned by Roper Technologies). The digital native insurgents that tried to dislodge the leaders in the 2010s have died - Convoy was probably best in class and collapsed in 2023. It is not obvious to me why Uber would have transformationally better tech than any of the other big players. Uber might take share from the tail, but CH Robinson has been doing that for decades and still “only” has 17% share.

In managed transport, while I can accept that customers are sticky, the same argument applies: I see no reason why Uber will be transformationally better than the competition, so while it might keep its existing customers, I do not understand why it should take share or have real pricing power. In addition we have no idea whether Uber is profitable within this segment. If it is, then brokerage is losing money hand over fist, which suggests brokerage is a much worse business than its peer CH Robinson.

I accept that the industry is in a downturn and Uber Freight have spent several years integrating an acquisition and rebuilding their technology. The business may well perform better in the next cycle. But have they built a platform for dominance? I don’t see it.

Where it gets interesting

There is one area where Uber Freight can genuinely do something different. By linking with Uber’s gig-economy driver network, Uber can add last-mile to its Freight offering. The long-run vision is a single platform that orchestrates first-mile, long-haul, and last-mile delivery across transport modes and geographies. This is virtually impossible for other freight brokers to replicate.

The problem is, I am not sure how many customers really need freight and last mile in the same package. Most users of freight are shipping from a factory to a warehouse or a retailer. And if they do need last-mile delivery direct to the customer, why would they choose Uber over or Amazon, which already offers consumer discovery, factory-to-doorstep logistics, trust, and returns all in one service?

That said, I do think there is a logic here. Direct to consumer is growing. By combining discovery and logistics, Uber can be a part of that trend. But a big, profitable part? Uber Freight has a lot to prove before we can conclude that.

Conclusion

Uber Freight operates in a large market where others have built profitable, capital light businesses. It may well become one of those. But there is very little evidence that it is a disruptive force, able to deliver materially greater efficiencies than competitors and take market share.

As an Uber shareholder I would absolutely love to be wrong on this. Do you think I am? Persuade me!

Links to previous work

Thanks for reading - if you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.