Review: Millrose Properties

Caveat emptor.

Summary

What it does: finances land banks for homebuilders

Elevator pitch: homebuilders want to go capital light. Millrose is happy to buy their land and sell it back to them when they need it, for a fee.

Mental model: n/a - I was hoping it would be value (read about my mental models here).

Valuation and potential returns: trades slightly below book value with a 10% yield. I think the upside is capped at 10% and the downside is significant.

Exchange and ticker: MRP, NYSE

Stock price and market cap: $31, $5.1bn

Do I own it? No.

IR website: here.

About this blog: I have been investing for 25 years, professionally and personally. I look for stocks that have a high probability of compounding at 15% for at least 5 years with limited downside. I write these stocks up on my blog. You can find more about me, my philosophy, my mental models, and my portfolio structure on my site.

Disclaimer: This post is for informational and educational purposes only. Building Arks is not licensed or regulated to provide any financial advisory service and nothing published by Building Arks should be taken as a recommendation to buy or sell securities, relied upon as financial advice, or treated as individual investment advice designed to meet your personal financial needs. You are advised to discuss your personal investment needs and options with qualified financial advisers. Building Arks uses information sources believed to be reliable, but does not guarantee the accuracy of the information in this post. The opinions expressed in this post are those of the publisher and are subject to change without notice. The publisher may or may not hold positions in the securities discussed in this post and may purchase or sell such positions without notice.

I meant to write about Microsoft this week, but got distracted by this. I don’t plan to write about stocks I don’t own very often, but I enjoyed thinking through this business model and the risks.

What it does

Millrose finances land banks for homebuilders. Homebuilders find a property they want; Millrose buys it; the homebuilder pays a deposit and an option premium; Millrose funds the development of horizontal infrastructure (roads, utilities, landscaping etc.); the homebuilder can then build and sell homes; and then, finally, the homebuilder exercises its option to buy the property.

How the finances work

Millrose’s P&L and balance sheet are almost completely separate (at least when things are going well - more on that later).

The P&L is quite simple. It looks like this: regular option premium payments, less management fees, less interest on debt, equals dividends. There is not much tax or retained earnings because Millrose is a REIT.

The balance sheet is also fairly simple: home sites on the asset side and equity + debt + deposits (in that order) on the liability side.

The cash flow statement is more interesting. Balance sheet activity creates massive inflows and outflows of cash. Millrose receives deposits, buys land, pays for horizontal infrastructure up to a pre-defined limit, and then sells the land at total cost. It looks like this:

In rough terms, the cost of the land and the cost of the basic infrastructure are about equal. I derive this from the fact that at year end Millrose had about $8bn of land on the balance sheet and will receive about $16bn if all options relating to that land are eventually exercised. The difference is the cost of developing basic infrastructure: another $8bn.

These asset cycling cash flows can be billions of dollars over a year. Because Millrose sells the land + infrastructure at cost, these transactions don’t usually touch the P&L. However, as we will see, there are real risks with this activity.

Why Millrose exists

Millrose was spun out of Lennar. It buys land from or for Lennar and other homebuilders. This allows the homebuilders to control a land bank without carrying it on their balance sheet. The idea is that the stock market rewards capital light businesses with higher valuations. This is true, but the market is not stupid (most of the time). It understands that in capital-heavy businesses, there is a cost, financial or strategic, to going capital light. And homebuilding is a fundamentally capital-heavy business: you can’t build homes without land, and the land needs to be good.

To go capital-light, therefore, homebuilders need to get land off their balance sheet while keeping access to it, keeping the economic upside of ownership, and transferring most of the risk. And that is exactly what Millrose lets them do.

Landbanking is not new. What’s new is listing a landbanking vehicle. Most landbanks are funds. They raise capital, buy land, sell it, and return the capital to investors. Millrose, being listed, doesn’t return the capital. Instead it recycles it into the next land acquisition. The other difference is that Millrose, being a REIT, taps into a large market of yield-hungry investors, particularly (I suspect) retirees. This may reduce the sophistication of Millrose’s investor base, and its cost of capital.

The bull case

Homebuilders are willing to pay 8-11% of the land value per year in option fees, which is sufficient for Millrose to pay a good dividend to its shareholders.

Millrose’s addressable market is theoretically huge. The value of the land and horizontal infrastructure underlying annual home starts in the US is $170bn. That’s all got to be on someone’s balance sheet, and why shouldn’t it be Millrose’s? The potential for growth seems huge. And indeed, according to management on results calls, homebuilders have been beating a path to Millrose’s door since the spin in early 2025.

A hard-asset company, trading at a discount to book value, yielding 10%, with a long runway for growth? What’s not to like?

Let’s find out.

The problems, in no particular order

Millrose pays Kennedy Lewis a management fee worth 1.25% of tangible capital. Not net tangible capital, and not tangible capital per share - just tangible capital. This seems to create two gloriously perverse incentives:

to issue cheap shares and buy expensive assets. There is some protection for the first 18 months post-spin, because Lennar kept a right to be compensated with extra shares if Millrose issued new shares below Lennar’s in-price. But once that date is past, I imagine the stock certificate printer at Millrose will go brrrrrrr. This might make it hard for the stock to rerate.

to carry assets at inflated valuations. Note that Millrose has not obtained an independent appraisal as to the value of its land. In effect, we have to trust the value that Lennar put on the land when it span Millrose out. Future acquisitions will be carried at cost (until they’re not).

Homebuilders sell land to Millrose, or bring Millrose ideas for land to buy. I think we can safely assume that they keep their best land on their balance sheet. There is a clear risk that they will dump their weaker assets on Millrose, and Kennedy Lewis will buy them to boost fees. Worse, Kennedy Lewis run traditional landbanking funds which compete with Millrose for acquisitions, so it is not even clear that the manager’s best deals will go into Millrose.

Millrose will struggle to grow book value or dividends per share. REITS have pay out most of their profits, so they can’t retain capital to grow. However most REITS do at least benefit from inflation in land prices and rents. Millrose does not: when they sell land, they only recoup their cost. Any land price inflation during Millrose’s ownership accrues to the homebuilder. Inflation protection is one of the main reasons to own real estate of any kind, and Millrose doesn’t offer it. This is one of the reasons Millrose’s yield is higher than most REITS: most REIT yields are implicitly inflation-linked (because underlying rents are expected to rise with inflation over time) but Millrose’s is not.

Millrose only has two ways to grow on a per share basis, and both are limited:

It can take on debt, but this adds risk and Millrose cap themselves at 33% debt-to-capital. They’re already at 25%.

It can shift its business mix away from Lennar towards other homebuilders, who pay higher options yields. However, Lennar has the right to reserve a significant part of Millrose’s capital. The exact calculation is complex, but the impact is that Millrose can’t grow its business with other homebuilders very much without issuing new shares. Since issuance may well be below book value, the resulting dilution is likely to offset the mix shift benefit.

Homebuilders don’t have to exercise options. They don’t even have to build homes on the land. If a project is uneconomic homebuilders can simply walk away. If they do, they lose their deposit and pay a termination fee, but in a major market downturn or if there are extreme project-specific issues walking away might be the economic or even the only option. It is inevitable that some options will not be exercised. In these cases, Millrose keeps the land but almost certainly loses money. They may be forced to sell the land for less than they paid, or worse: when a homebuilder walks, Millrose is liable for all the costs related to the land, which might include claims from unhappy homebuyers, the cost to remove partially-completed construction, or environmental reclamation costs.

In theory Millrose is protected from homebuilders walking away from options because land parcels are pooled: if a homebuilder walks away from one option it loses all the deposits in the pool, and Millrose can terminate the other options in the pool. Diversification within pools is meant to ensure that the assets aren’t correlated. Pooling ought to incentivise homebuilders to exercise, not walk, but it is imperfect:

Millrose cannot refuse to sell assets to Lennar, even if Millrose dispute Lennar’s right to buy based on pooling cross-termination provisions. All Millrose can do is litigate to recover losses. There is no guarantee this will succeed, and doing it could wreck Millrose’s relationship with their major customer. In addition, Lennar’s payments per pool appear to be capped, which presumably limits the value of the pooling provisions to Millrose.

When Millrose was spun out of Lennar, it was Lennar that chose which assets went into which pool. It is prudent to assume that they designed the pools to their benefit. Pooling offers little protection if all the bad assets are in one pool.

The following language appears in the 10k: “Lennar retains substantial discretion in selecting pool properties and setting pool terms. We may have limited ability to negotiate pooling conditions with Lennar…and we may not be able to negotiate pooling terms at all with Other Counterparties”. While this is to some extent boilerplate wording, it’s also true: pooling is by definition done through negotiation with homebuilders, who are not stupid. They will not accept pool terms that significantly increase their risks.

There are two implications of the homebuilder right to walk. The first is that far from growing, Millrose’s per share metrics are likely to decline over time. Millrose does not make a profit when a homebuilder exercises their option to buy a homesite - it simply gets back what it spent. But when a homebuilder does not exercise their option, Millrose is highly likely to take a loss. Millrose cannot offset inevitable losses on bad projects with profits on good ones. It can replenish the lost capital by issuing shares, but there is no incentive to do this above book value. Between losses on projects and share issuance below book value, it seems highly likely that book value per share will erode over time. And if book value per share erodes, so eventually must dividends per share, since the dividends are derived from asset ownership.

The second implication of the homebuilder right to walk is that Millrose has a potential cash flow timing mismatch which could be quite serious if there is a downturn or dislocation in the housing market. If homebuilders stop exercising their options, the cash inflow from selling land + horizontal infrastructure stops. However Millrose does not control the timing of the cash outflow to build horizontal infrastructure: if the homebuilder wants it built, Millrose has to fund it. Millrose could therefore face a situation where billions of dollars flow out but not in.

Millrose’s dividend is exposed to both housing market conditions and interest rates, which are likely to be somewhat correlated. Under some market conditions Lennar can suspend monthly option payments or reduce them by 50%. Other homebuilders may simply stop paying their option premiums. In addition, Millrose competes with alternative sources of finance. If interest rates fall, option premium rates on new deals must fall to remain competitive with debt finance. Millrose’s P&L is operationally and financially levered, so any reduction in option premiums will drive an even greater reduction in the dividend. Millrose’s dividend might behave more like a levered floating rate bond coupon than an equity dividend.

Finally, Millrose’s share structure means the company will never be subject to shareholder activism or sold to the highest bidder. Millrose has two classes of stock. The A shares trade publicly and have 1 vote per share. The B shares are 99% owned by the Miller family, which founded, runs, and effectively controls Lennar. Currently the B’s have 10 votes per share and 43% of the total votes. No matter how many A shares are issued, the B’s will never drop below 35% of total votes. Any amendment to Millrose’s Charter requires a 2/3rds supermajority, meaning in effect that the B’s have a veto. The Charter forbids anyone from owning more than 9% of Millrose unless exempted by the board - and anyway the B shares have a collective veto over various things, including a sale of the company.

Financial engineering

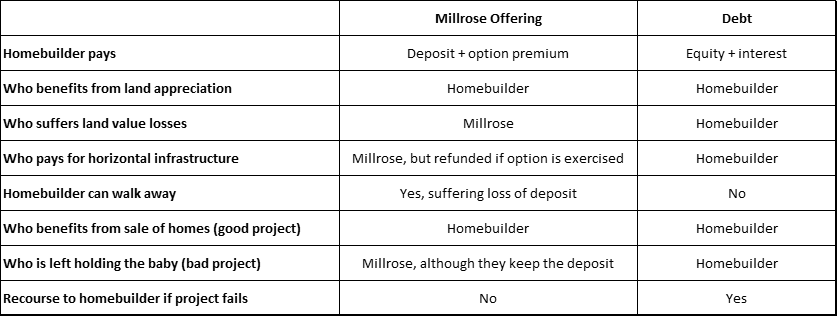

The comparison between the finance Millrose offers and the finance a lender offers is stark.

Option yields (premiums/land value) are 8-11%. Compared to debt, this seems like an expensive way to fund a land bank. However, the spread is significantly lower once you include Millrose’s significant investment in horizontal infrastructure, and it is arguably not adequate compensation for the additional risk Millrose takes compared to a lender.

How it could go wrong:

Kennedy Lewis grow Millrose as fast as possible, levering up and issuing shares to buy every land bank a homebuilder offers them without sufficient concern for downside risk.

The economy turns down and interest rates follow.

Some homebuilders stop exercising option contracts but Millrose still has to fund horizontal developments at the projects that are moving ahead. Cash makes a giant sucking sound.

To fund itself, Millrose sells land for whatever it can get. The company doesn’t take impairments, but it becomes clear its assets aren’t worth their marks. With leverage, mark-to-market book value is seriously impaired.

Lennar reduces its options payments by half. Rates come down so new deals, if there are any, are done at low yields. Millrose’s management fee and debt interest are fixed, however, so net income basically evaporates. The dividend is cut to 0. Panicked retirees rush for an increasingly crowded exit.

The stock drops 90%. Lennar offer a 20% premium to buy their land bank back for a song. There’s no counterbid because the Class B shares would veto it. Desperate shareholders vote for the deal.

This isn’t a prediction. But it wouldn’t be the first time, either.

Conclusion

Millrose yields 10%, but can’t grow value per share because it can’t retain profits. In fact, value per share is likely to decline in the long run because the manager has a strong incentive to issue shares below book value and because the company cannot offset the inevitable losses on some deals with gains on others. So the upside appears capped at +/- 10% per year, and that might be generous.

The potential downside, however, appears significant. There are protections in place such as pooling but the structure seems prone to a cashflow crisis, balance sheet impairments, and/or significant dividend reductions. I am not certain that any of these things will happen, but if they do, they may all happen at once.

On top of that, neither the manager nor the owner of supervoting shares seem well-aligned with Class A shareholders.

Contrast the risk/reward with Berkshire Hathaway, my go-to comparison stock. In my estimation Berkshire has a good chance of compounding intrinsic value at +/- 10% over time, so the upside is similar, but the chance of Berkshire becoming seriously impaired is vanishingly small. In fact, at just the sort of time when Millrose might become impaired, Berkshire is likely to be increasing its intrinsic value by buying assets on the cheap.

Also, a big part of investing is positioning yourself to make good decisions in tough times. With Berkshire, I know I won’t panic sell at the wrong time. With Millrose, I don’t.

There is only one way to find out whether this company will do well in a major downcycle: wait for one. I am happy not to own it while I do that.

Links to previous Reviews

Thanks for reading - if you enjoyed reading this please like and restack, and do get in touch if you have questions.

Pete

Great analysis, really enjoyed it. My view: the risks outweigh the returns.

The management fee structure alone would give me pause — 1.5% on gross tangible capital, not net, creates exactly the wrong incentives at exactly the wrong time. What this analysis surfaces that most Millrose coverage glosses over is the asymmetry of the homebuilder option: they get the upside of land appreciation, they can walk when projects go sideways, and Millrose is still on the hook for horizontal infrastructure costs regardless. That's not a land bank, that's a publicly traded entity absorbing the capital-heavy tail risk so Lennar can look capital-light on their balance sheet. The cashflow timing mismatch in a downcycle scenario is the piece that deserves more attention than it gets — the income stops before the obligations do, and that gap can move fast. For anyone drawn to the 10% yield, the honest question is whether you're being compensated for that specific risk or just for the illiquidity and complexity of understanding it. What's the actual bear case threshold where the dividend math breaks down — has anyone modeled a 20-30% option non-exercise rate?